For one reason or another, the owners decided to liquidate the LLC. How can an accountant plan the upcoming scope of work? And most importantly - what is the financial statements of such a company? Learn about it from our article.

Suppose the participants in a limited liability company (LLC) set out to liquidate it without resorting to bankruptcy. But even without it, the accountant will face many specific tasks. Among them is the preparation of two unusual balance sheets - an interim liquidation and liquidation.

Not every company has a full-time lawyer, and management, as usual, is in no hurry to attract specialists from outside. Therefore, on the eve of liquidation, most accountants have to independently study the Civil Code and other federal laws - first of all, “On Limited Liability Companies” (dated February 8, 1998 No. 14-FZ) and “On State Registration of Legal Entities and Individual Entrepreneurs” ( dated August 8, 2001 No. 129-FZ). Do not forget to also look into the charter of your LLC (clause 1, article 57 of Law No. 14-FZ)!

The head of an LLC is obliged to inform its participants about the occurrence of signs of bankruptcy (clause 1, article 30 of the Federal Law of October 26, 2002 No. 127-FZ “On Insolvency (Bankruptcy)”).

However, the liquidation process begins with the decision of the general meeting of participants and ends with an entry on the liquidation of the company in the Unified State Register of Legal Entities. The strategic plan for upcoming events is presented in the table.

| Stages of voluntary liquidation of an LLC (“cheat sheet” for an accountant) | |||

| No. p / p | Procedures | Sources of norms | Explanations |

| 1 | Liquidation is carried out by decision of the general meeting of participants. At the same time, a liquidation commission (LC) or a liquidator is appointed. | Law No. 14-FZ (clauses 1 and 2 of article 57, subparagraph 11 of clause 2 of article 33, clause 8 of article 37), the Civil Code of the Russian Federation (clause 2 of article 62) | The liquidation proposal may be made by the head of the LLC or its participant. The decision of the general meeting on liquidation must be unanimous. |

| 2 | The participants establish the procedure and terms for the liquidation of the LLC. All powers to manage the affairs of the LLC are transferred to the LC (including the fulfillment of the obligations of the LLC to creditors). | Civil Code of the Russian Federation (clauses 2 and 3 of article 62), appeal ruling of the Magadan Regional Court dated 15.05.2012 No. 33-460/2012 in case No. 2-8/2012 | The powers of the head of the LLC are terminated. He can be appointed the head of the LC or the liquidator. But this is already a function of a civil law nature. |

| 3 | It is necessary to submit to the registering body a "Notice on the liquidation of a legal entity" with the decision on liquidation attached. | Law No. 129-FZ (clause 1, article 20) | Notification form (No. Р15001) approved. Order of the Federal Tax Service of Russia dated January 25, 2012 No. ММВ-7-6/25. Information about the head of the liquidation commission (liquidator) is entered into it. |

| 4 | On the beginning of liquidation, the tax authorities make entries: - in the Unified State Register of Legal Entities; - in USRN. | Guidelines for tax authorities, approved. by order of the Federal Tax Service of Russia dated April 25, 2006 No. SAE-3-09 / 257 (section I) | From the moment the notification is submitted to the registration authority (f. No. P15001) and until the submission of the documents provided for in Art. 21 of Law No. 129-FZ, the tax authority is obliged to declare its requirements for the payment of all mandatory payments to the budget. |

| 5 | It is necessary to notify the authorities of the PFR and the FSS of the Russian Federation about the upcoming liquidation. | Federal Law No. 212-FZ dated July 24, 2009 (Signature 3, Clause 3, Article 28) | The form of the message is free. |

| 6 | In connection with the liquidation, it is possible: - field tax audit; - unscheduled field inspections of the PFR and the FSS of the Russian Federation. | Tax Code of the Russian Federation (clause 11, article 89), Law No. 212-FZ (clause 20, article 35) | Conducting inspections is a right, not an obligation, of the regulatory authorities (for example, paragraph 2 of the letter of the Ministry of Finance of Russia dated 03.12.2007 No. 03-05-05-05 / 05). |

| 7 | The LC publishes information about the beginning of the liquidation process in the journal State Registration Bulletin. | Civil Code of the Russian Federation (clause 1, article 63), order of the Federal Tax Service of Russia dated June 16, 2006 No. SAE-3-09 / 355 (clause 1) | The publication informs about the procedure and deadline for filing claims by creditors. This period cannot be less than two months from the date of publication. |

| 8 | In connection with the liquidation of the LLC, employees are subject to dismissal. They are warned about this personally and against signature at least two months before the dismissal. About the upcoming liquidation must be reported to the employment service. | Labor Code of the Russian Federation (clause 1, article 81, articles 178 and 180), Law of the Russian Federation of 04/19/1991 No. 1032-1 (clause 2, article 25) | A dismissed employee is paid a severance pay in the amount of the average monthly earnings, and he also retains the average monthly earnings for the period of employment, but not more than two months from the date of dismissal (including the severance pay). |

| 9 | OK: - identifies creditors and notifies them in writing of the liquidation of the LLC; - takes steps to collect receivables. | Civil Code of the Russian Federation (clause 1, article 63), resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 13.10.2011 No. 7075/11 | If the rights of the creditor are violated during the liquidation, the entry in the Unified State Register of Legal Entities on the termination of the activities of the LLC may be invalidated. |

| 10 | The LLC conducts an inventory of assets and liabilities (as of the date of the deadline for filing claims by creditors). | Federal Law No. 402-FZ dated 06.12.2011 (Article 11, subparagraph 4, paragraph 3, Article 21, paragraph 1, Article 30) | When an organization is liquidated, an inventory is mandatory (clause 27 of the Regulations on Accounting and Accounting in the Russian Federation, approved by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n). |

| 11 | After the expiration of the period for the presentation of claims by creditors, the LC draws up an interim liquidation balance sheet. It is approved by the founders (participants) of the LLC. | Civil Code of the Russian Federation (clause 2, article 63) | The “Notice on the liquidation of a legal entity” (form No. P15001) is submitted to the registering authority - “in connection with the preparation of an interim liquidation balance sheet”. You do not need to send the balance itself. |

| 12 | If the funds available to the LLC are insufficient to satisfy the requirements of creditors, then the LK sells the property at public auction. | Civil Code of the Russian Federation (clause 3, article 63), letter of the Ministry of Finance of Russia dated November 29, 2011 No. 03-02-07 / 1-410 | Trades are held in the manner established for the execution of court decisions (Chapter 9 of the Federal Law of 02.10.2007 No. 229-FZ). In connection with the sale of goods and property rights, taxes are paid on a general basis. ATTENTION! Settlements with creditors in kind are not provided for by law. |

| 13 | Information is submitted to the FIU (within one month from the date of approval of the interim liquidation balance sheet). | Federal Law No. 27-FZ of April 1, 1996 (clause 3, article 11), Law No. 129-FZ (subclause “d”, clause 1, article 21) | It is necessary to provide information on individual (personalized) records and a register of insured persons for whom additional insurance premiums have been paid for the funded part of the labor pension (clause 4, article 9 of the Federal Law of April 30, 2008 No. 56-FZ). |

| 14 | In case of insufficiency of property to satisfy the claims of creditors or if there are signs of bankruptcy of the company, the LK is obliged to apply to the arbitration court with an application for bankruptcy of the legal entity. | Civil Code of the Russian Federation (clause 3, article 63), Federal Law No. 127-FZ of October 26, 2002 (articles 224-226) | We do not consider liquidation through bankruptcy. ATTENTION! Supervision, financial recovery and external management in case of bankruptcy of a liquidated organization are not applied. |

| 15 | The obligation to pay tax ceases with the liquidation of the company after all settlements with the budget have been completed. | Tax Code of the Russian Federation (subclause 4, clause 3, article 44, article 49) | The LC fulfills the obligation to pay taxes (penalties, fines) at the expense of LLC funds, incl. received from the sale of his property. The tax period is determined in accordance with paragraphs. 3 and 4 art. 55 of the Tax Code of the Russian Federation. |

| 16 | After completion of settlements with creditors, the LC draws up a liquidation balance sheet. It is approved by the founders (participants) of the LLC. | Civil Code of the Russian Federation (clause 5, article 63) | The liquidation balance sheet is submitted to the registering authority (subparagraph “b”, paragraph 1, article 21 of Law No. 129-FZ). |

| 17 | The property of the company remaining after satisfaction of creditors' claims is transferred to its founders (participants). | Civil Code of the Russian Federation (clause 7, article 63), Tax Code of the Russian Federation (subclause 1, clause 2, article 43, clause 4, clause 1, article 251, clause 2, article 277) | The transfer of property to participants is not a sale (clause 1, article 39 of the Tax Code of the Russian Federation). On the taxation of settlements with participants - individuals, see letter of the Ministry of Finance of Russia dated 06.09.2010 No. 03-04-06 / 2-204. |

| 18 | Bank accounts are closed. | Civil Code of the Russian Federation (Clause 1, Article 859, Clause 3, Article 854), Tax Code of the Russian Federation (Signature 1, Clause 2, Article 23 of the Tax Code of the Russian Federation) | The bank account agreement is terminated at the request of the client at any time. Do not forget to report the closure of accounts to the IFTS. |

| 19 | The LC submits to the registration authority: - application for state registration of a legal entity in connection with its liquidation (f. No. Р16001); - liquidation balance sheet; - a document confirming the payment of the state fee; - a document confirming the submission to the FIU of information on contributions to compulsory social insurance of employees. | Law No. 129-FZ (clause 1, article 21) Application form approved. Order of the Federal Tax Service of Russia dated January 25, 2012 No. ММВ-7-6/25. | The application confirms that the procedure for liquidation of a legal entity established by federal law has been observed, settlements with its creditors have been completed and the issues of liquidation of a legal entity have been agreed with the relevant state bodies. The amount of the state duty is 800 rubles. (signature 3, clause 1, article 333.33 of the Tax Code of the Russian Federation). |

| 20 | The LK draws up the last financial statements of the liquidated legal entity. | Federal Law No. 402-FZ dated December 6, 2011 (Article 17) | There are no requirements for such reporting. |

| 21 | The LC organizes the ordering of archival documents and submits them to the state or municipal archive. | Federal Law No. 125-FZ of October 22, 2004 (clause 10, article 23), Order of the Ministry of Culture of Russia No. 558 of August 25, 2010 “On Approval of the “List of Typical Management Archival Documents…” | Upon liquidation of non-governmental organizations, documents on personnel, as well as archival documents, the terms of temporary storage of which have not expired, are transferred in an orderly state for storage to the state or municipal archive on the basis of an agreement between the LC and the relevant archive. |

| 22 | The registering authority publishes information on the liquidation of a legal entity in the State Registration Bulletin. | Law No. 129-FZ (clause 6, article 22) | The liquidation of a legal entity is considered completed, and the legal entity is considered to have ceased to exist after an entry about this is made in the Unified State Register of Legal Entities. |

Now you will be able to assess the upcoming "front of work" and even control the work of the lawyers who are assigned. Well, we will focus on the problems of accounting. So, you have to make:

note

If the owners change their mind about liquidating the LLC, then in order to stop the official procedure, you need to notify the registration authority. For this, the same form No. P14001 is used. Put a note in it “submitted in connection with the decision to cancel the earlier decision to liquidate the legal entity” and attach a new decision.

In connection with the decision to liquidate the company, it is necessary to review the accounting policy for accounting purposes. Why?

The fact is that the current accounting policy was formed on the basis of the assumption of business continuity. It implies that the company will continue to operate for the foreseeable future. She has no liquidation intentions, therefore, the obligations will be repaid in the prescribed manner (). Well, now the grounds for such an assumption are lost.

In what direction to revise the accounting policy - regulations do not explain. won't help us much. After all, it regulates the termination of part of the company's activities, and not the termination of a legal entity ().

What are the main changes in accounting policy? It is impossible to describe all the nuances in the article. We outline only the main directions. In the details, you will have to rely on your own professional judgment.

In the conditions of continuous operation, assets are divided into current and non-current, liabilities - into long-term and short-term. This principle of classification is enshrined in. The criterion is the term of circulation (repayment) - 12 months after the reporting date or the duration of the operating cycle, if it exceeds 12 months. But if less than 12 months are left before the liquidation of the company, such a classification loses its meaning.

This means that in sections I "Non-current assets" and IV "Long-term liabilities" of the standard balance sheet, dashes will have to be put.

Moreover, fixed assets (including profitable investments in tangible assets) and intangible assets cease to satisfy the conditions for their recognition ( and ). Accordingly, their depreciation stops. And the subsoil user will write off exploration assets (clause 21 of PBU 24/2011).

Due to the reclassification, you can open new synthetic accounts.

Example 1

In view of the liquidation, accounts 30 “Tangible assets intended for sale” and 31 “Tangible assets intended for distribution among owners” were introduced into the working chart of accounts of the LLC. The accountant wrote off tangible non-current assets to these accounts:

DEBIT 02 CREDIT 01, 03

Accumulated depreciation written off;

DEBIT 30 CREDIT 01, 03, 07, 08

Selected objects for sale;

DEBIT 31 CREDIT 01, 03, 07, 08

Objects have been allocated for transfer to the owners.

Loses the meaning and concept of financial investments (). It is advisable to sell these assets in advance, before the start of the liquidation procedure (). For example, debts on loans issued to special collection agencies. After all, the decision to liquidate, as a rule, is not sudden.

Similarly, one does not have to talk about materials in their normative sense (clause 42 of the Methodological Guidelines for Accounting for Inventories). After all, these commodity-material values are no longer subject to processing.

Based on the tasks facing the company, it is advisable to redistribute the assets into four groups:

Within the third and fourth groups, detailing is appropriate (for example, real estate, shares in the authorized capital of other companies, inventory, used equipment, etc.).

As part of the liability, it makes no sense to isolate the additional capital and the cost of own shares bought back from shareholders. These items are combined with retained earnings. The article “Deferred income” also loses its independent significance.

Finally, the balance sheet indicators "Deferred tax assets" and "Deferred tax liabilities" should be attributed to the line "Retained earnings (uncovered loss)".

In addition, the company's sales are no longer income from ordinary activities ().

If the receivables or payables are shown on your balance sheet at a discounted value (and the current rules allow such an assessment), then discounting should be abandoned in anticipation of liquidation. The reason is obvious: repayment deferrals are no longer available. Future calculations should be shown in nominal amounts.

It is possible that we will have to increase reserves for doubtful debts. After all, now you have a limited time to collect debts.

Undoubtedly, such a conditional indicator as business reputation () is subject to write-off. It will not generate cash flow. For the same reasons, the amounts on account 97 “Deferred expenses” are written off. After all, there is no “future” for your company. Transfer the corresponding amounts to the debit of account 91 “Other income and expenses”.

And it is advisable to bring the balance sheet value of assets as close as possible to the price of their possible sale.

How permissible is such "amateur activity" in accounting policy? - The purpose of reporting is to inform interested users who have to make economic decisions (). The above approaches will make reporting more informative. The company is no longer expected to have investors, so dynamic and historical approaches to assessing assets and liabilities are no longer relevant.

Features of financial statements during liquidation are described in. The reporting year of the company will be incomplete. It starts as usual - from January 1, but ends on the date preceding the date of making an entry on its liquidation in the Unified State Register of Legal Entities.

This reporting period is divided into two parts:

It turns out that the first period is covered by the liquidation balance sheet.

For the second period, the so-called last financial statements are compiled (). Moreover, it is said that the composition of the latest financial statements, the procedure for its preparation and the monetary measurement of objects in it should establish federal standards. But today there are none. For this reason, you are not required to draw up the “last financial statements”.

State statistical accounting requires data on the activities of companies for the entire reporting year, even if it is incomplete. It would seem that financial statements need to be generated and submitted for the entire period of the company's existence in the reporting year.

This conclusion follows directly from the relationship between the norms of Law No. 402-FZ. establishes that the annual accounts are prepared for the reporting year. And paragraph 1 of article 17 says that for a liquidated company, the reporting year is “shortened”. It is limited to the date of its existence.

At first glance, reporting is formed in a generally established manner. Meanwhile, the liquidation commission is not an economic entity that is obliged to compile and submit it to the state statistics body, and even at the place of state registration. After all, there is no such place. So it's not feasible. Similarly, there is no taxpayer (), therefore, there is no person obliged to submit reports for the last year to the tax office (again, it is not clear which one).

So before us is a “gaping hole” in the legislation. The most pleasant thing is that there is no one to punish for failure to submit reports. Regulatory authorities do not bother explaining themselves. The Federal Tax Service of Russia recommends compiling interim liquidation and liquidation balance sheets according to (approved by order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n). This letter was issued before the entry into force of the current accounting law ().

The requirement of civil law on the preparation of interim liquidation and liquidation balance sheets applies to credit institutions. This is confirmed by Article 23 (paragraph 12) of the Federal Law of December 2, 1990 No. 395-1 “On Banks and Banking Activities”. As you know, the accounting system of banks is carefully designed. Moreover, a bank may have the organizational and legal form of LLC (paragraph 1 of article 1 of Law No. 395-1). These considerations inspire the search for analogies ().

And indeed - there is a Regulation on the procedure for compiling and submitting an interim liquidation balance sheet and liquidation balance sheet of a liquidated credit institution (approved by the Bank of Russia on January 16, 2007 No. 301-P). Clause 1.2 of the Regulations states that the interim liquidation balance sheet and the liquidation balance sheet are drawn up in the form of a turnover sheet for accounting accounts as of the relevant date, indicating the period for which the corresponding balance sheet was drawn up.

It is noteworthy that this approach removes the issue of compiling for the period from the agenda. After all, SALT contains not only balance sheet accounts, but turnovers on income and expense accounts. But that's not all. Integral applications of these balance sheets are various interpretations. The balance is laced up with explanations to it. In particular, this is information about the amount of claims of creditors and the obligations of the company, information about the property (assets) of the company.

But most importantly, the incoming balances of the liquidation balance sheet must correspond to the outgoing balances of the interim liquidation balance sheet (clause 4.1.1 of the Regulations).

Interim liquidation balance sheet - a form of internal reporting, a working tool of the liquidation commission. It does not appear to external authorities. It is in it that it is necessary to apply the new accounting policies described above. This approach will make it possible to assess the financial position of the company with maximum realism. That is, to understand whether it has enough resources to meet the requirements of creditors (whether it is threatened with bankruptcy).

Recall: in the period between the dates of approval of the interim liquidation balance sheet and the liquidation balance sheet, payments are made to creditors. In this case, the sequence established must be observed. Moreover, payments to creditors of the third and fourth priority can be made only after a month has passed from the date of approval of the interim liquidation balance sheet.

An interim liquidation balance sheet can be drawn up on the expiration date for the presentation of claims by creditors ().

You are obligated to pay off only creditors who have submitted their claims before the deadline announced in the liquidation publication. You have the right to write off the debt of other creditors.

Please note: the document called "interim liquidation balance sheet" is not just a balance sheet. By virtue of paragraph 2 of Article 63 of the Civil Code, it must contain information:

The liquidation balance sheet is drawn up after settlements with creditors. The property remaining after satisfaction of their claims is transferred to the owners of the company (clauses 5 and 7 of article 63 of the Civil Code of the Russian Federation).

This distribution is made on the basis of Article 58 of Law No. 14-FZ. It also establishes a special order, namely:

The requirements of each queue are satisfied after the requirements of the previous queue are fully satisfied.

It may turn out that the property available to the company is not enough to pay the distributed but unpaid part of the profit. Then the property is distributed among its participants in proportion to their shares in the authorized capital of the company.

Example 2

There are two participants in the LLC, the shares of each of which in the authorized capital are 30% (legal entity) and 70% (individual). The size of the authorized capital is 100,000 rubles. According to the liquidation balance sheet, the undistributed profit of the company is 1,000,000 rubles.

There are no accounts payable, it is repaid.

Total liabilities - 1,100,000 rubles. (100,000 + 1,000,000).

That is, all liabilities are represented by equity.

Assets - cash in the amount of 1,100,000 rubles.

When making payments to participants, the LLC acts as a tax agent. Taxation does not include payments to a legal entity within the share of the authorized capital paid by him, that is, the amount of 30,000 rubles.

Taxes are subject to withholding and transfer to the budget at a "dividend" rate of 9%:

In this situation, the LLC accountant will apply the postings:

DEBIT 80 CREDIT 75

100 000 rub. - written off the authorized capital;

DEBIT 84 CREDIT 75

RUB 1,000,000 - distributed profit;

DEBIT 75 CREDIT 68

RUB 96,300 (27,000 + 69,300) - taxes withheld from participants' income;

DEBIT 68 CREDIT 51

RUB 96,300 - taxes withheld are listed;

DEBIT 75 CREDIT 51RUB 1,037,700 (1,100,000 - 96,300) - payments made to participants.

Balances on the liquidation date will be zero.

Summarize. During the liquidation of the company, the accountant becomes the most important figure. The company has practically no need for other employees. The role of the accountant is so great that it is advisable to include him in the liquidation commission.

Elena Dirkova, editorial board "PB", for the journal "Practical Accounting"

Accounting statements from balance sheet to explanatory note

All the necessary information for the correct preparation of any form of financial statements in the "Accounting Statements" Berator: a detailed line-by-line commentary for each form with examples of filling; recommendations for approval and reporting to the inspectorate.

Write-off of deferred expenses —procedure, the result of which is capable of affecting the financial position and financial performance of the firm. We will talk about the nuances of their write-off and the difficulties of classification in our article.

Future expenses or, as they are commonly called, deferred expenses (PBP) are expenses incurred by the company in past and (or) current periods and subject to write-off in subsequent time periods.

RBP are the object of accounting, although the mention of such a term is rarely found in accounting and tax regulations. For example, it is absent in the tax code, IFRS, the law of December 6, 2011 No. 402-FZ on accounting.

Based on the definition formulated by legislators in clause 65 of the accounting and reporting regulation, approved by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34, expenses incurred in the reporting period related to subsequent reporting periods are written off according to the scheme established for writing off the value of assets of this species during the time period to which they refer.

The classification of RBP and the definition of algorithms for their write-off is a procedure based on a detailed knowledge of the law and the practical experience of an accountant (financial specialist).

The absence in the legislation of a specific list of costs classified as RBP gives rise to a variety of approaches for accountants of different firms to reflect and write off RBP in accounting and reporting.

Since the set of costs incurred by different firms depends on the specifics of the activities of a particular firm, the nuances of recognizing RBP and the algorithm for their accounting may differ. These features are required to be provided for by including a separate section on this issue in the accounting policy.

When starting the process of classifying RBP, one should be guided by the requirements of the following regulatory documents:

More details about the costs that fall into the category of RBP on the basis of these groups of regulatory documents will be discussed in the next section.

It is safe to recognize the following costs as future expenses (since this is expressly stated in the legislation):

With regard to the remaining costs, which are written off evenly, their classification as part of the RBP requires a serious analytical approach from the accountant.

The main difficulty in this classification is whether the costs incurred should be treated as an asset or recognized as an expense? To help deal with this, the following algorithm can help classify costs as an asset:

At the same time, the firm is likely to have future economic benefits if it is possible to:

If the costs do not meet the criteria for an asset, they are recognized as an expense.

Correct classification will help to avoid errors in the reflection of RBP in the financial statements, as well as to apply the necessary method of writing them off.

To clarify this difficult task, officials of the Ministry of Finance of Russia gave the following explanations (letter dated 12.01.2012 No. 07-02-06 / 5):

Get acquainted with international approaches to asset valuation with the materials of our website:

After the RBP classification procedure has been carried out, their value is reflected in accounting and gradually written off using the following correspondence of accounts:

An important nuance in this case is the period of write-off of the RBP. If it is not specified in the contract, it is determined independently, taking into account the method of writing off the RBP fixed by the accounting policy. This method can be used:

When classifying future expenses and choosing a method for writing them off, not only knowledge of the nuances of the legislation on this issue is required, but also practical experience that allows the accountant to draw appropriate conclusions.

The algorithm called "Write-off of deferred expenses" is fixed in the accounting policy of the company.

Property inventory. In accordance with paragraph 2 of Art. 12 of Law No. 129-FZ, upon liquidation of an organization, before drawing up a liquidation (separation) balance sheet, it is necessary to conduct an inventory. The procedure for the inventory of property and financial obligations of the organization and registration of its results is established by the Methodological Guidelines for the inventory of property and financial obligations, approved by Order of the Ministry of Finance of Russia dated June 13, 1995 No. 49. accounting and verification of the completeness of the reflection in the accounting of liabilities.

Methodical instructions established the Rules for conducting an inventory. According to these Inventory Rules, all property of the organization, regardless of its location, and all types of financial obligations are subject to inventory.

In addition, inventories and other types of property that do not belong to the organization, but are listed in the accounting records (under safekeeping, leased, received for processing), as well as property not taken into account for any reason, are subject to inventory.

The inventory of property is carried out at its location.

Inventory rules include:

Inventory of property and financial obligations;

Inventory of fixed assets;

Inventory of intangible assets;

Inventory of financial investments;

Inventory of inventory items;

Inventory of work in progress and deferred expenses;

Inventory of animals and young animals;

Inventory of funds, monetary documents and forms of documents of strict accountability;

Inventory of settlements (settlements with banks and credit institutions for loans, settlements with the budget, buyers, suppliers, accountable persons, employees, depositors, other debtors and creditors), which consists in checking the validity of the amounts on accounting accounts;

Inventory of reserves for future expenses and payments, estimated reserves (the correctness and validity of the reserves created in the organization are checked: for the upcoming payment of vacations to employees; expenses for the repair of fixed assets; production costs for preparatory work due to the seasonal nature of production).

The property is inventoryed by its location and by the materially responsible person. For property, the inventory of which revealed deviations from the accounting data, collation statements are compiled. They reflect the results of the inventory, i.e. discrepancies between accounting indicators and inventory data.

Identified discrepancies between the actual availability of property and accounting data are reflected in the accounts in the following order.

Surplus property is accounted for at market value on the date of the inventory, and the corresponding amount is credited to the financial results of a commercial organization or an increase in income from a non-profit organization - Debit of property accounts (01, 03, 04, 08, etc.) Credit account. 91.1.

Loss of property and its damage include:

1) on the costs of production or circulation (expenses) within the norms of natural loss - Debit account. 20 (25, 26, 44, etc.) Credit account. 10, 41;

2) at the expense of the perpetrators (in excess of the norms) - Debit account. 94 Credit account 10, 41;

3) if the perpetrators are not identified or the court refused to recover losses from them, then these losses are written off to the financial results of a commercial organization or an increase in expenses of a non-profit organization - Debit account. 91.2 Credit account 94.

If the surplus accounted for at market value in accordance with paragraph 5 of Art. 274 of the Tax Code of the Russian Federation, increase the tax base for income tax as non-operating income (clause 20 of article 250 of the Tax Code of the Russian Federation), then expenses in the form of a shortage of material assets in production and in warehouses, at trade enterprises in the absence of guilty persons, as well as losses from theft, the perpetrators of which have not been identified, can be recognized as a reduction in the tax base only if the fact of the absence of perpetrators is documented by an authorized state authority (clause 5, clause 2, article 265 of the Tax Code of the Russian Federation).

With the further implementation of the inventory surplus identified as a result of the inventory for the purposes of taxation of profits, the organization will be able to recognize expenses in the amount of income tax calculated from income, which was reflected in tax accounting when posting the identified surpluses (clause 2 of article 254 of the Tax Code of the Russian Federation).

Example. As a result of the inventory of goods and materials in the warehouse, a shortage of 50 meters of cotton fabric at a price of 100 rubles was revealed. per meter and excess linen fabric in the amount of 40 meters at a price of 150 rubles. per metre. The persons responsible for the shortage have not been identified; on the basis of the order of the liquidation commission, the shortage is attributed to the losses of the organization. There are no documents from authorized state authorities confirming the absence of perpetrators. The revealed surpluses of fabric are realized in the process of liquidation. In accounting, the results of the inventory are reflected in the following entries: Debit account. 94 Credit account 10 - 5000 rubles. - reflects the shortage of cotton fabricDebit c. 19 Credit account 68.2 - 900 rubles. - restored VAT, previously accepted for deductionDebit c. 94 Credit account 19 - 900 rubles. – VAT is charged to the account of shortageDebit account. 91.2 Credit account 94 - 5900 rubles. - shortages are charged to expensesDebit account. 10 Credit account 91.1 - 6000 rubles. - capitalized surplus linen fabric Debit c. 62 Credit account 91.1 - 7080 rubles. - sold surplus linen fabricDebit c. 91.2 Credit account 10 - 6000 rubles. - the cost of the sold fabric is debited. 91.2 Credit account 68.2 - 1080 rubles. - VAT has been charged. Only 6,000 rubles can be accepted as a reduction in the tax base for income tax when selling capitalized surpluses. x 24% = 1440 rubles.

An inventory is subject not only to the property of the organization, but also to its obligations (settlements with the budget, with accountable persons, with payroll personnel, with debtors and creditors, etc.). The procedure for reconciling taxpayers' settlements of taxes and fees is established by Order of the Federal Tax Service of Russia dated 09.09.2005 No. SAE-3-01 / [email protected]"On Approval of the Regulations for the Organization of Work with Taxpayers, Payers of Fees, Insurance Contributions for Compulsory Pension Insurance and Tax Agents". The rules for reconciliation of taxpayers' settlements set forth in this document shall apply starting from 01.11.2005.

Write-off of the cost of fixed assets. The procedure for liquidation and write-off of fixed assets from the balance sheet is established by paragraphs 94 - 97 of the Methodological Guidelines for the accounting of fixed assets, approved by Order of the Ministry of Finance of Russia dated 20.07.1998 No. 33n.

1. Creation of the commission.

To determine the expediency and unsuitability of fixed assets for further use, the impossibility or inefficiency of their restoration, as well as to draw up documentation for the write-off of these items in the organization (if the availability of fixed assets is significant), a permanent commission may be created by order of the head, which includes relevant officials, including the chief accountant (accountant) and persons who are responsible for the safety of fixed assets. Representatives of relevant inspections may be invited to participate in the work of the commission.

2. Drawing up an act for the write-off of fixed assets.

The results of the decision taken by the commission are documented in an act for the write-off of fixed assets. Decree of the State Statistics Committee of Russia No. 7 dated January 21, 2003 approved new forms of primary accounting documentation for accounting for fixed assets.

The following forms are used to register and record the write-off of fixed assets that have become unusable:

Act on the write-off of an object of fixed assets (except for motor vehicles) - form No. OS-4;

Act on the write-off of vehicles - form No. OS-4a;

The act of writing off groups of fixed assets (except for motor vehicles) - form No. OS-4b.

The act is drawn up in two copies, signed by members of the commission appointed by the head of the organization, and approved by the head or a person authorized by him. The first copy is transferred to the accounting department, the second remains with the person responsible for the safety of fixed assets, and is the basis for the delivery to the warehouse and the sale of material assets and scrap metal remaining as a result of the write-off. When a vehicle is written off to the accounting department, along with the act, a document is transmitted confirming its deregistration in the State Inspectorate for Road Safety of the Ministry of Internal Affairs of Russia (Gosavtoinspektsii).

The costs of writing off fixed assets, as well as the cost of tangible assets received from the dismantling of fixed assets, are reflected:

a) in section 3 "Information on the costs associated with the write-off of an object of fixed assets from accounting, and on the receipt of material assets from their write-off" (form No. OS-4);

b) in section 5 "Information on the costs associated with the write-off of vehicles from accounting, and on the receipt of material assets from their write-off" (form No. OS-4a);

c) in section 2 "Information on the receipt of material assets from the write-off of fixed assets" (form No. OS-4b).

3. Posting of material assets.

Parts, components and assemblies of dismantled and dismantled equipment suitable for the repair of other fixed assets, as well as other materials are accounted for as scrap or scrap at market value, and unusable parts and materials are accounted for as secondary raw materials and are reflected in the debit of the materials accounting account in correspondence with financial results account.

4. Mark in the inventory card (book).

On the basis of acts for the write-off of fixed or motor vehicles transferred to the accounting service of the organization, a mark on the disposal of the object is made in the inventory card (inventory book). Corresponding entries on the disposal of an item of fixed assets are also made in a document opened at its location.

Acceptance, movement of fixed assets within the organization, including reconstruction, modernization, overhaul, as well as their disposal or write-off are reflected in the inventory card (book) on the basis of relevant documents.

Inventory cards for retired fixed assets are kept for a period determined by the head of the organization.

According to clause 101 of the Methodological Guidelines for the Accounting of Fixed Assets, the write-off of the value of fixed assets is reflected in accounting on a detailed basis: in the debit of the write-off (sale) of fixed assets - the initial cost of the object, recorded on the account of fixed assets, and the costs associated with disposal fixed assets that are preliminarily accumulated on the auxiliary production cost account (accrued wages and social insurance contributions made for employees involved in fixed asset retirement operations, taxes and fees paid from proceeds from the sale of fixed assets, etc.), and on the credit of the specified account - the amount of accrued depreciation charges, the amount of proceeds from the sale of valuables related to fixed assets.

Income, expenses and losses from write-offs from the balance sheet of fixed assets are reflected in the accounting records in the reporting period to which they relate. Income, expenses and losses from the write-off of fixed assets from the balance sheet are subject to crediting from the write-off (realization) accounting account to the financial results of the organization (clause 103 of the Methodological Instructions).

According to paragraph 75 of the Guidelines on the procedure for the formation of financial statements of an organization, approved by Order of the Ministry of Finance of Russia dated June 28, 2000 No. 60n, expenses associated with the write-off of fixed assets, including their residual value, are accounted for as other expenses:

- in case of write-off due to obsolescence and physical depreciation of fixed assets;

– in case of write-off as a result of accidents, natural disasters and other emergencies.

Incomes in the form of tangible assets remaining after the write-off of fixed assets are recognized as part of other income, respectively.

In accounting, the write-off of an object of fixed assets is reflected in the following entries:

Debit 01 "Disposal of fixed assets" Credit 01 - reflects the initial (replacement) cost of the decommissioned item of fixed assets;

Debit 02 Credit 01 "Retirement of fixed assets" - the amount of accrued depreciation was written off;

Debit 91-2 Credit 01 “Retirement of fixed assets” - the residual value of the fixed asset was written off;

Debit 91-2 Credit 23 (25, 69, 70, other accounts) - the costs associated with the liquidation (write-off) of the fixed asset were written off;

Debit 10 Credit 91-1 - tangible assets left over from the write-off of the fixed asset object (at market value) were credited.

And today we will touch on the topic write-offs of deferred expenses. Let me remind you that deferred expenses are one-time costs that should be included in the expenses of the organization in subsequent reporting periods. In this article, we will consider some of the theoretical features of this concept, as well as the mechanisms for accounting for such expenses in 1C BUH.

Separately, I note that I will consider not only the program settings regarding the routine operation of closing the month "Write-off of future expenses", but also for the purposes of forming balance sheet. And of course, as usual, we will consider everything in examples and colorful screenshots.

Let me remind you that the site already has a number of articles that are devoted to the issue of closing the month in the 1C BUKH 3.0 program:

To account for deferred expenses (RBP) in the chart of accounts, there is account 97 “Deferred expenses”. It has sub-accounts, which are subdivided depending on the type of expense:

As analytics, these sub-accounts use the elements of the 1C BUH "Deferred expenses" directory. But we will talk about this in more detail later in the examples.

There is a situation when it is required to carry out equal write-offs of insurance payments (for example, for voluntary insurance), but not to consider such a payment as RBP. In this case, account 76 “Settlements with different debtors and creditors” should be used, namely two sub-accounts:

We will also consider the use of these sub-accounts in a separate example.

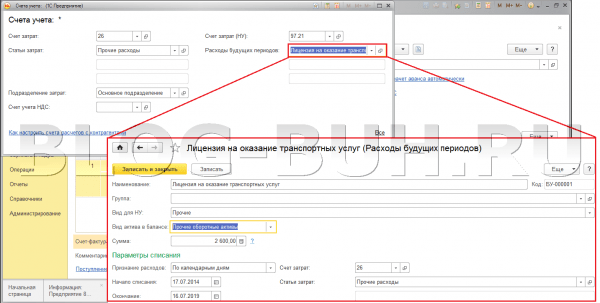

In the example, the organization receives a license for the provision of transport services for a period of 5 years, for which a state duty of 2,600 rubles has been paid. We will reflect the acceptance for accounting of expenses for paying for a license using the document “Receipt of goods and services”. For the document, select the type of operation "Services". When filling out the document, the most important thing is to correctly indicate the field of the tabular part of the account. According to the conditions of our example, we select account 26 “General business expenses” as the cost account, since in accounting the costs will be written off immediately. But in tax accounting we will use deferred expenses, therefore we will select account 97.21 “Other deferred expenses” in the appropriate field. If you use RBP in both accounting and tax accounting, then instead of 26 we naturally choose 97.

As I wrote earlier, 97 accounts have elements of the "Deferred expenses" directory as analytics. Let's create an element in this directory that will fit our case. The two most important fields here are "Type of asset in the balance sheet" and "Expense recognition". The second field affects how the balance on account 97 will be written off at the end of the month. There is a calculation option "By months", "By calendar days" and "In a special order". We will select "By calendar days" - the calculation is carried out in proportion to the number of days in a month. I'll explain a little later.

The values in the “Type of asset in the balance sheet” field determine which line of the balance sheet this expense will be included in. The following values are possible:

If for some element of this directory the type of asset is not filled in, then when forming the balance sheet, it will be assigned to line No. 1260 “Other current assets”. Of course, only if it has a debit balance on account 97.

For our example, we will select the value “Other current assets” in this field.

Now let's post the document and see the postings.

So we have two wires. In the first, costs are written off as expenses of the organization to account 26 in accounting. The second entry in tax accounting generates RBP on account 97. A temporary difference between accounting and tax accounting is also formed.

Now let's perform the regulated month-end closing operation "Write-off of deferred expenses" and see the generated postings.

Expenses from account 97.21 are written off to 26 "General expenses". We see that the postings are generated only in tax accounting, which is true in our example. There is also an amount that covers the temporary difference. As for the amount itself, let me remind you that we have chosen “By calendar days” as the parameter for writing off deferred expenses. The amount to be debited in July is calculated by the formula:

2 600 rub. / (365+366+365+365+365) * 15 = 2,600 rubles. / 1,826 (calendar days for 5 years) * 15 (from July 17 to July 31) = 21.36 rubles.

For August, the amount will be larger since we will calculate for a full month:

2 600 rub. / (365 + 366 + 365 + 365 + 365) * 31 \u003d 2,600 rubles. / 1,826 (calendar days for 5 years) * 31 (all of August) = 44.14 rubles.

We will select the type of document “Other write-off”, and as the debit account 76.01.2 “Payments (contributions) for voluntary insurance in case of death and injury to health”. This account has the element of the reference book "Expenses of future periods" as the second subconto. Therefore, we will create the desired element and select it in the corresponding field of the document. RBP will be in the amount of 18,000 rubles. and for a period of 1 year, and the method of writing off by months.

During the execution, the following postings will be generated:

At the close of the month during the year, the entire amount will be debited to the expenses of the organization.

The write-off amount will be calculated using the following formula:

18 000 rub. / 12 months = 1,500 rubles.

However, due to the fact that the payment was made on July 17 in the middle of the month, the first and last months will be calculated in proportion to the days:

18 000 rub. / 12 * (15 / 31) = 725.81 rubles.

That's all for today! If you liked this article, you can use social media buttons to keep it for yourself!

Also don't forget your questions and comments. leave in the comments!

Accounting account 97 is used to reflect generalized information on the amounts of expenses actually incurred in the current reporting period, but relating to future periods. How to take into account deferred expenses and what transactions reflect operations on account 97 - you will find answers to these questions in our article.

Deferred expenses are preparatory costs incurred by the organization to generate income in the future. According to legislative norms, the debit of account 97 can reflect expenses for:

The grounds for the reflection of amounts as part of deferred expenses are primary documents confirming the fact of receipt of income in the future (contract agreement, license agreement, etc.).

The amounts of deferred expenses are accumulated under Dt 97, the write-off of expenses and their reduction is reflected under Kt 97.

Expenses for reflection on account 97 can be recognized as the costs incurred by the organization for the repair of fixed assets and intangible assets:

Goods, materials, finished products can be written off for expenses of future periods:

One of the most common operations on account 97 is the reflection of deferred expenses associated with the conclusion of license agreements for the use of software.

Consider an example: in August 2015, Molniya LLC signed a license agreement with Computer Service JSC. Under the agreement, Molniya LLC receives the rights to use the software for a period of 3 years. The cost of the contract is a one-time payment in the amount of 342,500 rubles.

The following entries were made in the accounting of Molniya LLC:

| Dt | ct | Description | Sum | Document |

| Funds were transferred in favor of Computer Service LLC as payment under a license agreement | RUB 342,500 | Payment order | ||

| 97 | The cost of the contract is included in deferred expenses | RUB 342,500 | License agreement | |

| 012 | Software accounted for on the off-balance sheet | RUB 342,500 | License agreement | |

| 20 ( , 44…) | 97 | Monthly write-off of expenses for the use of software (342,500 rubles / 36 months) | RUB 9,514 | License agreement |

Deferred expenses may include costs under a construction contract. Expenses can be posted to account 97, provided that their amount is accurately and reliably determined, and there is also a possibility of concluding a contract for construction work.

Consider an example: Mega Stroy LLC is preparing for a tender for the construction of a residential complex. The start of the tender is August 2015. In February 2015, in order to prepare a feasibility study (feasibility study) for the project, Mega Stroy LLC enters into an agreement with Designer LLC, the cost of services for which is 894,000 rubles, VAT 136,372 rubles. The contractor delivers the work in April 2015.