Dmitry Mironov Site Manager

Consider an example of recording transactions by a tax agent.

Document: Receipt of goods and services.

Operation type: Purchase, commission.

Menu: Purchase.

The contract of the counterparty must necessarily indicate that the Organization acts as a tax agent. As well as the type of agency agreement. In our case, this is "Non-resident".

The program automatically generates a posting in the credit of account 76.NA

Document

Operation type: Supplier payment.

Menu: Bank

To facilitate document entry, you can use the "Enter based" function

We enter the article of the movement Money, we'll need it at the end of the quarter.

After the bank writes off funds from the current account, we form the document “Write-off from the current account”. To do this, follow the link

"Enter a debit document from the current account"

Document: Tax agent invoice. It is formed using the Tax Agent Invoice Registration.

Menu Purchase - Keeping a book of purchases. We select the period for which we need to generate invoices, and click the "Fill" button.

After filling in the tabular part, you need to click the "Run" button.

This processing generates the document Invoice issued with the type Tax agent.

The invoice, in turn, generates a transaction for closing an account 76.NA.

And gets into the sales book.

Document: Payment order, Write-off from the current account.

Operation type: Tax transfer

Menu: Bank

Be sure to check the box "Transfer to the budget"

Forming a write-off from the current account.

We indicate the account on which the debt was formed - 68.32, fill in the counterparty, the contract and the document of settlements with counterparties. The main thing here is not to make mistakes, because the settlement document is a payment order, according to which we transferred funds to the supplier. To accurately indicate the settlement document, you can generate an OSV on account 68.32

After filling in all the lines, we carry out the document.

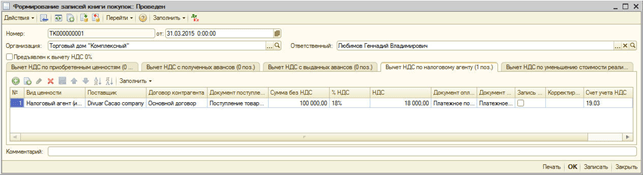

Document: Formation of the book of purchases.

Menu: Purchasing - Keeping a book of purchases.

By clicking the "Fill" button, the deduction is automatically filled.

When posting the document, postings are generated for offsetting VAT.

And a shopping book.

Value added tax is paid when selling goods, works, services on the territory of Russia when applying common system taxation for an organization and OSNO for an individual entrepreneur.

However, in the process economic activity the enterprise may have situations when the supplier - VAT payer, cannot pay tax to the budget of the Russian Federation. In this case, the buyer acts as a tax agent for payment of VAT to the budget.

All these situations are described in article 161 of the Tax Code of the Russian Federation (part 2; section 8; chapter 21):

The fulfillment of the duties of a tax agent in the event of the above situations is assigned both to VAT payers and to persons and organizations applying special tax regimes, as well as those exempted from paying this tax (Article 145 of the Tax Code of the Russian Federation).

When making payment, partial payment, prepayment to the supplier, the invoice of the tax agent is registered - the documents “Debit from the current account” with the operation “Payment to the supplier” are entered into the 1C system, and the “Invoice received” generated on the basis of this document with an operation code of the form "06" - Tax agent, art. 161 NK. For certain transactions, for example, if the buyer acts as a tax agent under municipal property lease agreements, tax agent invoices are generated by special processing.

When posted, the document will make movements on account 68.32 “VAT in the performance of duties of a tax agent” and on the accumulation register “VAT Sales”.

The delivered goods, work, service are accepted for accounting with the buyer; the previously paid advance payment to the supplier is accepted for offset - the document “Receipt (acts, invoices)” is generated, the invoice presented by the supplier (if required) is registered by hyperlink in the receipt document.

The VAT presented by the supplier was transferred by the tax agent to the budget of the Russian Federation - the document “Write-off from the current account” was generated with the operation “Payment of tax”.

Of course, the described scheme is too general, and for different business transactions, in which the enterprise acts as a tax agent, there are different solutions in the 1C system, but the format of this article does not imply consideration of all possible situations and their implementation in 1C software products.

Let us consider in more detail the operation for the sale of raw animal skins, aluminum and its alloys, scrap and waste of non-ferrous metals, since this is a new provision of Article 161 of the Tax Code of the Russian Federation, which comes into force on January 1, 2018.

From this date, all buyers, with the exception of individuals who are not individual entrepreneurs, when purchasing raw hides and scrap in Russia from organizations paying VAT (if they have not received an exemption from VAT), are tax agents for this tax.

VAT is calculated by the tax agent at the estimated tax rate. The amount of VAT to be paid to the budget is determined in aggregate, based on the sum of all transactions of the tax agent for the past tax period.

The moment of definition tax base for such payers is:

How this operation implemented in 1C 8.3?

Let's open the section "Reference books" / subsection "Purchases and Sales" / "Agreements". In the card of the counterparty agreement with the type of agreement “With a supplier”, we will configure the “VAT” part:

Postings on advance payment transactions are formed in the system by debiting documents from the current account in the section "Bank and cash desk" / subsection "Bank" / magazine "Bank statements".

The document "Write-off from the settlement account" generates a posting on the debit of account 60.02 and the credit of account 51 for the amount of the advance payment transferred to the supplier.

At the time the supplier receives payment for the upcoming supply of scrap metal, the buyer must fulfill the duties of a tax agent for calculating VAT, and the seller must issue an invoice for the advance payment received, excluding VAT amounts, with the note “VAT is calculated by the tax agent”.

To register this operation, it is necessary to enter the document "Invoice received" on the basis of the document "Debit from the current account". The document will show:

Note, that for this operation the VAT of the tax agent is recorded on account 68.52 “VAT of the tax agent for certain types of goods” (clause 8 of article 161 of the Tax Code of the Russian Federation).

At the same time, entries are made in the registers "Invoice Logbook", "VAT Sales" and "VAT Purchases" to store information about the received invoice, indicating the type of value and event.

To reflect the receipt document, crediting the advance to the supplier and accounting for incoming VAT, we use the document "Receipt (act, invoice)" with the type of operation "Goods (invoice)". The document can be issued in the section "Purchases" / subsection "Purchases" / "Receipt (acts, invoices)".

Let's create a new document and fill it in according to the data received from the supplier. When posting a document, the accounting register reflects the entries for offsetting the advance to the supplier, the cost of scrap metal received from the supplier and the amounts of VAT calculated by the tax agent for the seller, based on the amount of delivery.

In the register "VAT presented" will be added records for the type of movement "Arrival". In this case, the value "Goods (tax agent)" will be reflected in the "Type of value" field.

According to Art. 168 (p. 5) of the Tax Code of the Russian Federation, the supplier-payer of VAT when shipping non-ferrous metal scrap is obliged to issue an invoice to the buyer.

After recording the invoice received, postings are generated on account 76.NA - for the amount of VAT calculated by the buyer-tax agent for the supplier from the cost of delivery, and an entry will appear in the "VAT Sales" register indicating the type of value "Goods (tax agent)" and "VAT accrued payable" event.

Scrap metal is taken into account. Now the buyer-tax agent has the right to a tax deduction for VAT:

If all transactions during the period are performed without errors and "manual" adjustments, the regulatory VAT documents "Formation of sales book entries" and "Formation of purchase book entries" are generated automatically by clicking "Fill". For convenience, users can use the "VAT Assistant" in the section "Operations" / subsection "Closing period".

After the regular operations of VAT reflection in the purchase book and in the sales book, entries will appear on transactions:

Since the amount of tax payable to the budget for buyers of non-ferrous metal scrap, who are tax agents, is calculated as total amount, increased by the restored VAT and reduced by the amounts tax deductions(details can be found in Article 170-0172 of the Tax Code of the Russian Federation), in our example, the amount payable will be 0 rubles:

The amount of VAT calculated by the buyer - tax agent - 27,000 rubles.

The amount of VAT for which the buyer-tax agent has the right to deduct is 27,000 rubles.

Filling order tax return on VAT obliges tax agents to fill in section 2 of the declaration. But section 2 does not ensure compliance with the control ratios of indicators (this requirement is contained in the letter of the Federal Tax Service of the Russian Federation No. GD-4-3 / [email protected] from 03/23/2015).

For taxable items - sales book entries

We considered the reflection of accounting operations for the activities of a tax agent in the 1C system.

In accordance with Art. 161 of the Tax Code of the Russian Federation, organizations can act as tax agents.

The program automates the following cases when organizations can act as tax agents:

Tax agents are required to calculate, withhold from the taxpayer and pay the appropriate amount of VAT to the budget. This section uses an example to consider the reflection of business operations of an organization in the performance of the duties of a tax agent when purchasing goods from a foreign organization that is not registered with the tax authorities of the Russian Federation.

To record transactions, do the following:

1. Registration of an agreement with the performance of the duties of a tax agent.

Let's register the contract in the directory "Contracts of counterparties":

2. Transfer of advance payment

To do this, you need to register the document "Outgoing payment order" (menu "Documents - Cash").

3. Registration of issued invoice

When transferring payment to a supplier under an agreement with the performance of the duties of a tax agent, an invoice must be issued.

An invoice can be generated automatically by processing "Registration of tax agent invoices" (menu "VAT - Registration of tax agent invoices") or entered manually on the basis of a payment document.

The formation of tax agent invoices and their posting is carried out by clicking the "Execute" button. When processing is performed, invoices are created and the data of invoices created earlier is updated.

When posting invoices of a tax agent, the amounts of VAT payable to the budget are accrued: an entry in the debit of account 76.NA "Calculations for VAT in the performance of duties of a tax agent" and credit of account 68.32 "VAT in the performance of duties of a tax agent".

The amount of VAT charged is reflected in the sales book.

In the invoice, the nomenclature is filled with a generalized name from the contract. The name of the item can be specified in the invoice manually.

4. Posting goods

Let's register the document "Receipt of goods and services" with the type of operation "Purchase, commission" (menu "Documents - Purchases"). To offset the advance payment with the supplier, we will process "Restoring the sequence of settlements with counterparties" (menu "Documents - Advanced").

Wires are generated:

5. Transfer of VAT to the budget

The fact of transferring VAT to the budget is registered by the document "Outgoing payment order" with the type of transaction "Tax transfer" (menu "Documents - Cash").

The document must indicate the counterparty, the contract and the settlement document by which the transfer of payment to the supplier was executed.

6. Registration of the VAT amount in the purchase book

Purchase book entries for VAT amounts deductible when performing the duties of a tax agent are reflected in the "Creating Purchase Book Entries" document on the "VAT Deduction by Tax Agent" tab. The tabular part is automatically filled in by clicking the "Fill" button.

When conducting, postings are formed:

For illegal non-withholding and (or) non-transfer of tax amounts by a tax agent, a tax sanction is provided - a fine of 20% of the tax amount. To avoid tax sanctions, check your counterparties and transactions with them.

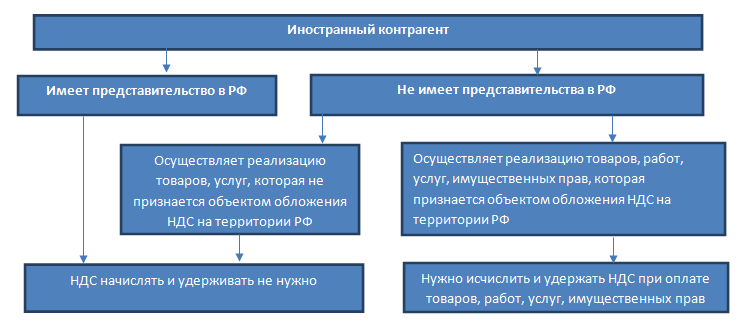

Below is a diagram that will help you figure out who is considered a VAT tax agent.

Article 161 of the Tax Code of the Russian Federation describes situations when a tax agent calculates and pays to the budget for a VAT payer. Consider the two most popular situations.

To confirm that you do not have the duties of a tax agent, it is best to request a copy of the certificate of tax registration (indicating the TIN and KPP) of the representative office of a foreign organization in Russia.

At the same time, if the buyer concludes a contract with the head office of a foreign company (a branch registered in the Russian Federation does not take part in the transaction), then the buyer must fulfill the duties of a tax agent, despite the fact that a representative office is registered in the Russian Federation (letter of the Ministry of Finance of Russia dated 11/12/2014 No. 03-07-08/57178).

If a foreign organization sells goods, works, services that are not recognized as subject to VAT in Russia, then the buyer does not need to calculate and withhold VAT.

The withholding tax from a payment to a foreign organization is calculated using the formula:

Example. A foreign organization provides information services to a Russian organization. In accordance with Art. 148 of the Tax Code of the Russian Federation, the Russian Federation is recognized as the territory for the provision of services. Foreign partners did not submit a certificate of registration with the tax authority in the Russian Federation. The cost of the service is 100,000 rubles. The Russian organization is obliged to withhold VAT when paying for services. The amount of VAT will be 100,000 * 18/118 = 15,254.24 rubles. “In hand” the contractor under the contract will receive 84,745.76 rubles.

Often, foreign contractors indicate in contracts that they want to receive a certain fixed amount of money for their goods, work, services, and all taxes payable in Russia, the buyer must accrue in excess of the specified amount and pay at his own expense.

Such wording in the agreements does not affect the procedure for the tax agent to perform its functions and does not prevent the receipt of a deduction in respect of VAT paid to the budget under such an agreement.

In some cases Russian organizations are required to withhold from payments to foreign companies not only VAT, but also income tax (Article 309 of the Tax Code of the Russian Federation). If an organization is both a tax agent for both VAT and income tax, then taxes are calculated as follows: first, VAT must be calculated and withheld, and then income tax, excluding the amount of VAT from the tax base.

For example, Russian company pays a foreign company the cost property rights 100,000 euros for the use of the developed site. VAT = 100,000 *18/118 = 15,254.24 euros. Income tax = (100,000 -15,254.24) * 20% = €16,949.15. Tax amounts are recalculated into rubles at the exchange rate as of the date of transfer to the budget (Article 45 of the Tax Code of the Russian Federation). Please note that the tax rate on the income of a foreign organization depends on an international agreement on the avoidance of double taxation between Russian Federation and the country where the foreign counterparty is a resident. The agreement may provide for the exemption of income of a foreign organization from taxation in the territory of the Russian Federation or taxation at a reduced tax rate. If there is no such agreement between the states, then the rate of 20% should be applied.

According to article 312 of the Tax Code of the Russian Federation, in order to apply the exemption from taxation of income of a foreign company in the territory of the Russian Federation or the application reduced rates tax documentary evidence is required:

Residence in a country with which Russia has concluded an international agreement on the avoidance of double taxation;

The actual right to dispose of the income received under the agreement (in particular, confirmation that the counterparty is not an intermediary).

Supporting documents must be provided by the foreign organization to the withholding agent prior to the income payment date.

1) Landlord - city administration, management committee state property, municipality or other similar body (bilateral agreement). In this case, the tenant is recognized as a tax agent.

2) The lessor is the city administration, the state property management committee, the municipality or other similar body, the balance holder is a unitary institution (tripartite agreement). In this case, the tenant is also recognized as a tax agent.

3) Landlord - a municipal or federal unitary institution (school, hospital, bus station, etc.). Such institutions are independent taxpayers. The tenant is not a tax agent.

4) The lessor is a state institution. The services of such institutions are not subject to VAT. The tenant is not a tax agent.

If the tenant is a tax agent, then he is obliged to calculate VAT at the time of payment rent. The tax amount is determined as follows:

The same deadlines are set for the transfer to the budget of VAT accrued in relation to the rent for the use of state / municipal property.

In practice, it is more convenient for a tax agent when making any purchase to transfer VAT to the budget at the time of payment under an agreement with a foreigner or government agency/ municipality. This will avoid technical errors, which means avoiding the accrual of penalties and fines for late transfer of tax to the budget. In addition, the payment period affects the period for deducting the amount of VAT paid to the budget by the tax agent.

In lines 2, 2a, 2b of the invoice, the tax agent indicates the details of the seller / lessor. In line 2b (TIN and KPP) of the invoice, dashes are entered if the seller is a foreign organization. In line 5 of the invoice, in the case of the purchase of works, services from a foreign organization, the tax agent must indicate the number and date of the payment order by which VAT was transferred to the budget.

Mandatory conditions for accepting VAT for deduction:

1) there are payment documents confirming the payment of VAT to the budget;

2) goods (works, services) for their use in activities subject to VAT;

3) there is an invoice issued by you (the tax agent);

4) purchased goods (works, services) are taken into account. VAT deductible can be accepted in the same period in which VAT was paid to the budget, subject to other mandatory conditions.

Example: the organization rents premises from the municipality to accommodate an office for 300,000 rubles. per month. The amount of VAT is 300,000 * 18/118 = 45,762.71 rubles. The share of transactions subject to VAT is 5% of the total revenue (clause 4, article 170 of the Tax Code of the Russian Federation). On March 30, the organization transfers 254,237.29 rubles to the budget. on account of rent for March and 45,762.71 rubles. towards the payment of VAT. In accounting, the corresponding accruals of rent were made. When generating a declaration for the 1st quarter, the organization will reflect: - accrual of tax payable as a tax agent 45,762.71 rubles, - the amount of VAT deductible 2,288.14 rubles. (45762.71 *5%). The difference between VAT paid to the budget and VAT accepted for deduction (RUB 43,474.57) will be taken into account by the organization when calculating income tax as part of the cost of renting premises.

Thus, by concluding an agreement with a foreign organization or authority (municipality), the organization (entrepreneur) assumes additional functions and responsibilities. For planning purposes tax implications before signing an agreement with an “unusual” counterparty, you should first investigate its status, assess how its status will affect the calculation of taxes, and stock up necessary documents and confirmations.

The tax agent's VAT is taken into account if:

purchase of goods is carried out in foreign currency from a non-resident;

the property is leased;

property is for sale.

Accounts 76.HA and 68.32 are used to account for VAT. We propose to analyze all three situations and determine the peculiarity of the invoice.

The main condition for the purchase of goods in foreign currency from a non-resident is the correct completion of the contract parameters:

Type of contract - indicate "With a supplier";

The organization acts as a tax agent for the payment of VAT - check the box;

Type of agency agreement - indicate, "Non-resident".

We process the receipt of goods in a standard way, but without registering an invoice:

In the movement of the document, subaccount 76.HA will be used, and not the usual mutual settlement account.

To reflect VAT, special processing will be used, which can be found on the menu tab "Bank and cash desk" section "Registration of invoices" magazine "Invoices of the tax agent":

We open the form. It is only necessary to set the period and the name of the agent organization (if the 1C program is used for accounting of several companies at the same time, for example, when using 1C online remotely). The filling is automatic by clicking "Fill", while the tabular part will display all the necessary documents.

By clicking "Run", invoices will be generated and registered:

In the form of an invoice, let's pay attention to the specified VAT rate - "18/118" and the designation of the operation code - 06.

Postings will reflect special accounts 76.HA and 68.32, which are added to the chart of accounts:

The VAT amount for mandatory payment to the budget is checked through the Sales Book report and through the VAT Declaration document. The "Sales book" report is generated in the "VAT reports" section.

At the same time, the period of formation and the name of the taxpayer organization are indicated:

The formation of the VAT declaration is carried out in the "Reporting" section, the item "Regulated reports", "VAT declaration". The value of the amount for payment will be reflected on page 1 section 2 in line 060:

The tax is paid through model documents 1C programs "Payment order" and "Debit from the current account", in which the "Type of operation" - "Payment of tax" must be indicated.

Please note that for the correct write-off of VAT, you must specify account 68.32.

After that, we accept VAT deduction. Go to the menu tab "Operations" section " Scheduled Operations VAT".

We create the document "Formation of purchase book entries" and open the "Tax agent" tab:

We post the document and watch the movement on the document "Formation of purchase book entries":

Then we proceed to the formation of the "Purchase Book" document, which is located in the "VAT Reports" section. The column "Name of the seller" will appear not the agent organization, but the seller organization:

If you view the declaration, then on page 1 section 3 of term 180 you can see the value of the amount to be deducted for the operation of the tax agent:

The sale of property through a tax agent is formalized with an indication of the correct type of contract and in compliance with the OS accounting rules:

Below is the sequence of registration for the accounting of invoices by a tax agent:

creation of an agency agreement;

posting of goods or services with the specified contract;

payment for goods or services to a supplier

registration of the invoice of the tax agent;

payment of VAT to the budget;

acceptance of VAT for deduction through the document "Formation of purchase book entries".