Definition

Absolute (cash) liquidity ratio(cash ratio) shows the ratio of the most liquid assets of the organization - Money about and short-term financial investments - to short-term obligations.

The absolute liquidity ratio is a variation of two other more common liquidity ratios: the ratio current liquidity and quick liquidity ratio. At the same time, only the fastest-selling (liquid) assets are used in the calculation of this indicator.

Calculation (formula)

The coefficient is calculated as follows:

Absolute liquidity ratio = (Cash + Short-term financial investments) / Current liabilities

All components of the formula are taken from the balance sheet of the organization.

Normal value

The absolute liquidity ratio is not as popular as the current and quick liquidity ratios and does not have a well-established norm. Most often, a value of 0.2 or more is used as a guideline for the normal value of the indicator. However, a too high value of the coefficient indicates an unreasonably high amount of free cash that could be used for business development.

Read about the cash liquidity ratio in English in the article " Cash Ratio".

Definition

Current (total) liquidity ratio(current ratio) is a measure of the solvency of the organization, the ability to repay the current (up to a year) obligations of the organization. Lenders widely use this ratio in assessing the current financial position of the organization, the risk of issuing short-term loans to it. In Western practice, the ratio is also known as the working capital ratio.

Calculation (formula)

The current liquidity ratio is calculated as the ratio of current assets to short-term liabilities:

Current liquidity ratio = current assets/ Short-term liabilities

The numerator of the formula is taken from the balance sheet asset, the denominator - from the liability.

Normal value

The higher the value of the current liquidity ratio, the higher the liquidity of the company's assets. A coefficient value of 2 or more is considered normal. However, in world practice, it is allowed to reduce this indicator for some industries to 1.5.

A low value of the coefficient (below 1) indicates that the organization is likely to have difficulties in repaying its current liabilities. However, to complete the picture, you need to look at the cash flow from the organization's operations - often a low ratio is justified by a strong cash flow (for example, in fast food chains, retail).

Too high current ratio is also undesirable, since it may reflect insufficiently efficient use of current assets or short-term financing. In any case, lenders prefer to see a higher ratio as a sign of a company's soundness.

Read about the current liquidity ratio in English in the article " Cash Ratio".

Quick ratio

Definition

Quick liquidity ratio(quick ratio, acid-test ratio) characterizes the organization's ability to pay off its short-term liabilities through the sale of liquid assets. At the same time, liquid assets in this case include both cash and short-term financial investments, as well as short-term receivables (according to another version, all current assets, except for their least liquid part - stocks). The quick liquidity ratio has become widespread in Russian and world practice along with the current liquidity ratio.

Calculation (formula)

Quick liquidity ratio is calculated by dividing liquid assets by short-term liabilities:

Quick ratio = (Cash + Short-term financial investments+ Short term accounts receivable) / Short-term liabilities

According to another version:

Quick liquidity ratio = (Current assets - Stocks) / Current liabilities

Inventories are considered to be the least liquid assets, they are considered the most difficult to convert into money (ie, to sell), so they are not included in the calculation anyway.

Normal value

The higher the quick liquidity ratio, the better the financial position of the company. A value of 1.0 or higher is considered normal. At the same time, the value may differ for different industries. If the ratio is less than 1, liquid assets do not cover short-term liabilities, which means that there is a risk of loss of solvency, which is a negative signal for investors.

Using the absolute liquidity ratio, it is determined what part of immediate debts can be repaid at the expense of cash and their analogues (securities, bank deposits etc.). That is, through highly liquid assets.

The absolute liquidity ratio, along with other liquidity indicators, is of interest not only to the management of the organization, but also to external subjects of analysis. So, this ratio is important for investors, quick liquidity - for banks; and absolute - to suppliers of raw materials and materials.

Absolute liquidity shows the short-term solvency of the organization: whether the company is able to pay off its obligations (with counterparties-suppliers) through the most liquid assets (money and cash equivalents). The coefficient is calculated as the ratio financial resources to current liabilities.

The standard calculation formula looks like this:

Cubs. = (cash + short-term cash investments) / current liabilities

Cubs. = highly liquid assets / (most current liabilities + medium-term liabilities)

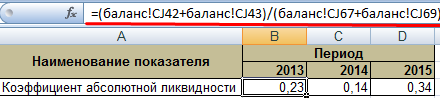

The data for calculating the indicator are taken from the balance sheet. Consider an example in Excel.

We circled the lines that are needed to calculate the absolute liquidity ratio. Balance formula:

Cubs. = (p. 1240 + p. 1250) / (p. 1520 + p. 1510).

Calculation example in Excel:

Just substitute the values of the corresponding cells (in the form of links) into the formula.

Accepted in foreign practice normative value coefficient - > 0.2. The essence of the restriction: every day the company must repay at least 20% of current liabilities. Practice financial analysis in Russian companies adheres to the same principles. However, there is no justification for such an approach.

The structure of short-term debt in Russian practice is heterogeneous. Repayment terms vary considerably. Therefore, the figure 0.2 should be considered insufficient. For many enterprises, the coefficient rate is in the range of 0.2-0.5.

If the absolute liquidity ratio is below the norm:

A large increase in the absolute liquidity ratio shows:

Thus, the higher the indicator, the higher the liquidity of the company. But excessively high values indicate the irrational use of funds: the enterprise has an impressive amount of finance that is not “invested in the business”.

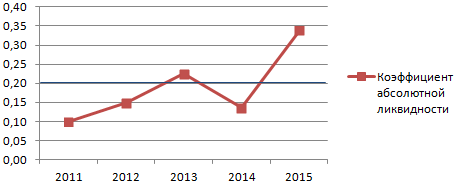

Let's go back to our example.

The values of absolute liquidity in 2013 and 2015 are within the normal range. And in 2014, the company experienced difficulties with the repayment of short-term liabilities.

Let us illustrate the dynamics of the indicator and for good example display on the chart:

To make a complete analysis of the solvency of the enterprise, all indicators of the liquid current assets of the organization are calculated. This ratio is used to calculate the share of short-term liabilities that can be repaid immediately. The example shows that the value for the period 2011-2015. increased by 0.24. In 2011, 2012 and 2014 the company experienced solvency difficulties. But the situation has normalized - the company is able to fulfill its current obligations by 34%.

The financial ratio you get dividing cash and short-term financial investments into short-term liabilities. The data for the calculation is the balance sheet of the company.

It is calculated in the FinEkAnalysis program in the solvency analysis block.

Shows what proportion of short-term debt obligations will be covered by cash and cash equivalents in the form of marketable securities and deposits, i.е. absolutely liquid assets.

Liquidity ratios are of interest to the management of the enterprise and for external subjects of analysis:

The general formula for calculating the coefficient:

Calculation formula according to the old balance sheet:

where p.250, p.260, p.610, p.620, p.660- lines of the balance sheet (form No. 1)

A1 - the most liquid assets; P1 - the most urgent obligations; P2 - short-term liabilities

Calculation formula according to the new balance sheet:

The normative limit K al > 0.2 means that at least 20% of the company's short-term liabilities are subject to repayment every day. The specified normative restriction is used in foreign practice of financial analysis. At the same time, there is no exact justification why, in order to maintain a normal level of liquidity, Russian companies the amount of cash should cover 20% of current liabilities.

In Russian practice, there is a heterogeneity in the structure of current liabilities and their maturity, so the normative value is insufficient. For Russian companies, the normative value of the absolute liquidity ratio is in the range K al > 0.2-0.5.

Was the page helpful?

"Liquidity" is the ability of some assets of a particular enterprise to quickly transform (transform) into other types of assets that are currently more in demand.

The most precise concept of "liquidity" is defined by a unit of time during which an asset is transformed, usually into cash.

Liquidity at the enterprise, in fact, shows its ability to cover its obligations. That is why they separate assets that are sold for a certain (average) period at a market price and assets for which the deadlines for execution are clearly indicated.

The liquidity of an enterprise, first of all, shows its ability to cover short-term liabilities for working capital. The liquidity ratio gives the most accurate and general idea of the liquidity of a company's assets. In order for an enterprise to have a normal level of liquidity, a necessary condition is the excess of the value of assets over the current amount of liabilities (“golden financial rule”).

“Current liquidity ratio” (or as it is also called “general debt coverage ratio”) is an analytical indicator that is based on the calculation of the ratio between current assets and short-term (current) liabilities.

The current liquidity ratio shows how quickly and to what extent an enterprise can pay off its short-term debts (with a maturity of no more than one year). In this case, current assets with a certain market value act as a source of financing liabilities.

The higher the current liquidity indicator, the more stable the situation at the enterprise, since its solvency is higher. At the same time, experts mean not only the current solvency at a certain point, but also the company's ability to pay its bills in the face of a sharp change in external financial circumstances that cannot be influenced.

The appearance of some force majeure may force the company's management to sell part of the reserves. This kind of activity is not the main profile of the company. The basis for calculating the current liquidity indicator is the company's balance sheet ( accounting form number 1).

Having calculated the indicator of current liquidity, it is necessary to interpret it correctly.

Having calculated the indicator of current liquidity, it is necessary to interpret it correctly.

If the coefficient value is below 1.5, then this is a direct evidence that the company has some difficulties in covering its current liabilities.

However, this situation can be resolved by obtaining sufficient cash flow in the course of the company's operations. To do this, the expert needs to analyze the “Cash Flow Statement” (in form No. 4), line 4111. For example, for firms that are engaged in retail trade, this situation is quite acceptable.

An overestimated liquidity indicator often indicates insufficient use of working capital and limited access to short-term loans (including bank loans). For example, the accumulation of illiquid goods on a completely profitable company is characterized by a rapid increase in the current liquidity ratio.

Among other factors that may lead to an increase in the liquidity ratio, the following are distinguished:

Liquidity - ease of sale, sale, transformation of material or other values into cash to cover current financial obligations.

Liquidity ratios - financial indicators, calculated on the basis of the company's statements (balance sheet of the company - form No. 1) to determine the company's ability to repay current debt at the expense of existing current (current) assets. The meaning of these indicators is to compare the amount of current debts of the enterprise and its working capital, which should ensure the repayment of these debts.

Consider the main liquidity ratios and formulas for their calculation:

Calculation of liquidity ratios allows you to analyze the liquidity of the enterprise, i.e. analysis of the possibility for the enterprise to cover all its financial obligations.

Note that the assets of the enterprise are reflected in the balance sheet and have different liquidity. Let's rank them in descending order, depending on the degree of their liquidity:

Current liquidity ratio or Coverage ratio or General liquidity ratio - a financial ratio equal to the ratio of current (current) assets to short-term liabilities (current liabilities). The source of data is the company's balance sheet (Form No. 1). The coefficient is calculated by the formula:

Current liquidity ratio = Current assets, excluding long-term receivables / Current liabilitiesKtl = (p. 290 - p. 230) / p. 690 or

Ktl = p. 290 / (p. 610 + p. 620 + p. 660)Ktl = line 1200 / (line 1520 + line 1510 + line 1550)

The ratio reflects the company's ability to repay current (short-term) liabilities at the expense of current assets only. The higher the indicator, the better the solvency of the enterprise. Current liquidity ratio characterize the solvency of the enterprise not only at the moment, but also in case of emergency.

The normal value of the coefficient is from 1.5 to 2.5, depending on the industry. Both low and high ratios are unfavorable. A value below 1 indicates a high financial risk associated with the fact that the company is not able to consistently pay current bills. A value greater than 3 may indicate an irrational capital structure. But at the same time, it must be taken into account that, depending on the field of activity, the structure and quality of assets, etc., the value of the coefficient can vary greatly.

It should be noted that this ratio does not always give a complete picture. Typically, firms with low inventories and easily obtainable bills of exchange can easily operate at a lower ratio than firms with large inventories and sales of goods on credit.

Another way to check the sufficiency of current assets is to calculate urgent liquidity. Banks, suppliers, shareholders are interested in this indicator, since the company may face circumstances in which it will immediately have to pay some unforeseen expenses. It means that she will need all her cash, securities, receivables and other means of payment, that is, part of the assets that can be turned into cash.

The ratio characterizes the company's ability to repay current (short-term) liabilities at the expense of current assets. It is similar to the current liquidity ratio, but differs from it in that the working capital used for its calculation includes only highly - and medium liquid current assets (money in operating accounts, stock of liquid materials and raw materials, goods and finished products, receivables from short term repayment).

Such assets do not include work in progress, as well as inventories of special components, materials and semi-finished products. The source of data is the company's balance sheet in the same way as for current liquidity, but inventories are not taken into account as assets, since if they are forced to be sold, losses will be maximum among all current assets:

Quick liquidity ratio = (Cash + Short-term financial investments + Short-term receivables) / Current liabilities

Quick liquidity ratio = (Current assets - Stocks) / Short-term liabilities

Kbl = (p. 240 + p. 250 + p. 260) / (p. 610 + p. 620 + p. 660)

Kbl = (p. 1230 + p. 1240 + p. 1250) / (p. 1520 + p. 1510 + p. 1550)

This is one of the important financial ratios that shows what part of the company's short-term liabilities can be immediately repaid from funds in various accounts, in short-term securities, as well as receipts from settlements with debtors. The higher the indicator, the better the solvency of the enterprise. The normal value of the coefficient is more than 0.8 (some analysts consider the optimal value of the coefficient 0.6-1.0), which means that cash and future receipts from current activities should cover the current debts of the organization.

To increase the level of urgent liquidity, organizations should take measures aimed at increasing their own working capital and attracting long-term loans and borrowings. On the other hand, a value of more than 3 may indicate an irrational capital structure, this may be due to the slow turnover of funds invested in inventories, the growth of receivables.

In this regard, the absolute liquidity ratio, which should be more than 0.2, can serve as a litmus test of current solvency. The absolute liquidity ratio shows what part of the short-term debt the organization can repay in the near future at the expense of the most liquid assets (cash and short-term securities).

A financial ratio equal to the ratio of cash and short-term financial investments to short-term liabilities (current liabilities). The data source is the company's balance sheet in the same way as for current liquidity, but only cash and cash equivalents are taken into account as assets, the calculation formula is as follows:

Absolute liquidity ratio = (Cash + Short-term financial investments) / Current liabilities

Cab = (p. 250 + p. 260) / (p. 610 + p. 620 + p. 660)

Cab = (p. 1240 + p. 1250) / (p. 1520 + p. 1510 + p. 1550)

A coefficient value of more than 0.2 is considered normal. The higher the indicator, the better the solvency of the enterprise. On the other hand, high rate may indicate an irrational capital structure, an excessively high proportion of non-performing assets in the form of cash and funds in accounts.

In other words, if the balance of funds is maintained at the level of the reporting date (mainly by ensuring a uniform receipt of payments from counterparties), short-term debt for reporting date can be repaid in five days. The above regulatory limitation is applied in foreign practice of financial analysis. At the same time, an exact justification why, in order to maintain a normal level of liquidity Russian organizations the amount of cash should cover 20% of current liabilities, not available.

Net working capital is required to maintain financial stability enterprises. Net working capital is defined as the difference between current assets and short-term liabilities, including short-term borrowings, accounts payable obligations equated to it. Net working capital is a part of working capital formed from own working capital and long-term borrowed capital, including quasi-own capital, borrowed funds and other long-term liabilities. The formula for calculating net settlement capital is:

Net Working Capital = Current Assets - Current Liabilities

Chob = p. 290 - p. 690

Chob = p. 1200 - p. 1500

Net working capital is necessary to maintain the financial stability of the enterprise, since the excess of working capital over short-term liabilities means that the enterprise can not only pay off its short-term liabilities, but also has reserves for expanding activities. Net working capital must be above zero.

The lack of working capital indicates the inability of the company to repay short-term obligations in a timely manner. A significant excess of net working capital over the optimal need indicates the irrational use of enterprise resources.

Formulas for calculating liquidity ratios in accordance with international standards described in