The state in order to support the ongoing population policy fixed in the tax legislation a kind of benefit: a tax deduction for personal income tax for children. Why is personal income tax taken or income tax? Because this is exactly the obligation that almost all citizens fulfill before the state. Russian Federation with the exception of pensioners - no income tax is withheld from the pension.

Like all other benefits, the provision of tax deductions is carried out exclusively through an application from the applicant. It must be written to the accounting department of the enterprise where the parent is officially employed. The tax deduction is equally granted to both the father and the mother in a single amount established by tax legislation. If the child is raised by one parent, then the deduction based on the submitted application will be provided in double the amount.

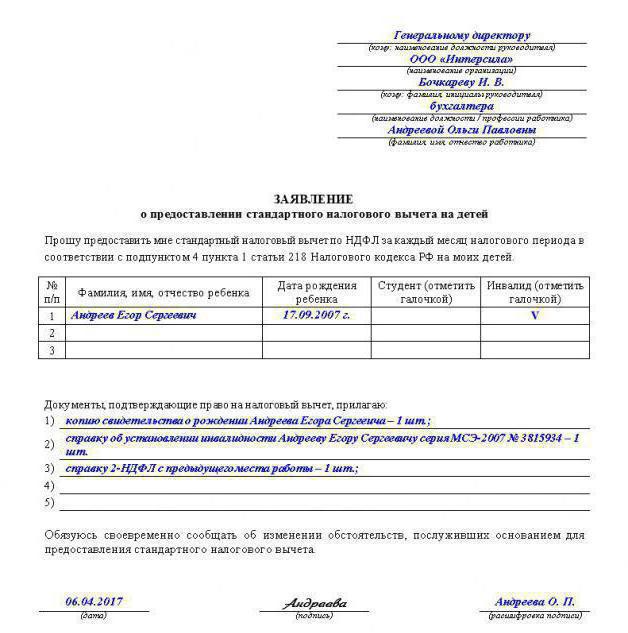

A standard sample application for a tax deduction for children can be obtained from the accounting department. Otherwise, the application can be made in free form, indicating the following details and personal data:

Attention! Applications for granting a deduction are written annually! There is no deduction for a child over 24, even if they continue to study full-time!

The application must be accompanied by a package of supporting documents for the tax deduction for children. These will be:

The deduction sizes are different:

I would like to note that these tax benefits are provided not only to biological parents, but also to any legal representative: guardian, foster parent, adoptive parent.

In order to determine the amount of the deduction for the second or third child, do not forget that all born and adopted children are taken into account, regardless of age. If the oldest of the three children is already 25 years old, then who, for example, is 16 years old, will be provided in the amount of 3,000 rubles. Therefore, it is important for the applicant to list all children (regardless of age) in the application for the child tax credit. A sample of such information may not contain.

So, summarizing all of the above, we note the following:

The Tax Code of the Russian Federation provides for several types of tax deductions. Among them are standard ones, provided in connection with a certain status of a citizen or marital status. Parents, adoptive parents, guardians and trustees can use the privilege.

The amount depends on the number of children, the state of their health, whether the taxpayer is raising them alone or is married, and by whom he is related minor child: parent or guardian. In 2020, the following tax benefits have been established:

Benefits are summed up, for example, if a citizen has three minor descendants, he will receive 1,400 rubles for the first and second, 3,000 rubles for the third, the amount of compensation will be 5,800 rubles.

Single parents get double the benefit!

Parents, adoptive parents, guardians and trustees (and their spouses) whose children:

You can use the benefit by submitting an application for a deduction for a child directly to the employer, since he is his tax agent and on his behalf transfers the amount of personal income tax to the budget.

If a citizen has not applied for a preference to the employer, you can get it through the Federal Tax Service. This can be done at the end of the calendar year by submitting a 3-NDFL declaration and a certificate of income in the form 2-NDFL.

An application for a benefit submitted to an employer must be supported by the following documents:

The term for granting benefits is limited - it is provided to a citizen until such time as his total income for the current calendar year will not reach 350,000 rubles. Starting from the month when the income exceeded this limit, the relief is terminated.

The legislation does not provide for a unified application form for a standard tax deduction for children. You can make it in any form, but it must be in writing. Include the following information:

Director

GBOU DOD SDYUSSHOR "ALLURE"

Ivanov I.I.

from a riding instructor

Petrova P.P.

STATEMENT

Based on paragraph 4 of part 1 of Art. 218 of the Tax Code of the Russian Federation, I ask you to provide me with a standard tax deduction for personal income tax due to the fact that I have a minor dependent Anatoly Petrovich Petrov, born on January 30, 2005.

I attach the following documents to the application confirming the right to receive a tax benefit:

Each officially employed worker has personal income tax withheld from his salary. However, the law allows the use of small benefits in calculating this tax, which are expressed as standard deductions. The most commonly used deduction is per child. To qualify, you must submit applications for the 2019 standard child tax credit.

For such a statement, there is no mandatory form. Most often, the accountant provides the employee with a template in which he just needs to deliver data about himself. Another option for compiling a document is to provide the employee with a sample on the basis of which he will write his application.

First, at the top of the sheet, it is indicated to whom the application is sent - the name of the position of the head of the business entity, the name of the entity itself, after that, full name. leader. All the above information must be written in the dative case.

Next, in the middle of a new line, the name of the form is indicated - “Application”.

The text of the application must include a request from the employee to the employer to provide him with standard deductions for his child or children.

The text must necessarily mention the article from the Tax Code, which regulates the provision of these benefits - for example, "in accordance with paragraph 4, paragraph 1, Article 218 of the Tax Code of the Russian Federation."

Next, you need to list all the children for whom the deduction request is made. It is desirable to do this in the form of a list, in each line of which the full name should be indicated. child, date of birth and the amount of the requested deduction.

Following is a list of documents that will be attached to the application and confirm the legitimacy of the requested benefits. Such forms include a copy of a birth certificate, a certificate of guardianship, a certificate of disability, and others.

In the case when an employee is employed not from the beginning of the calendar year (and this usually happens rarely), but in the middle of it, then he, most likely, already enjoyed benefits at the previous place of work.

Therefore, to confirm the amount of earnings from the previous place, he needs to provide a 2-personal income tax certificate. It should also be mentioned as an attachment to the application.

The preparation of the application is completed by indicating the date and affixing the signature of the employee.

Free consultation of our lawyer

Do you need expert advice on benefits, subsidies, payments, pensions? Call, all consultations are absolutely free

Moscow and region

7 499 350-44-07

St. Petersburg and the region

7 812 309-43-30

Free in Russia

A large number of taxpayers are trying to find a way to reduce the revenue side when calculating government fees. The legal norms of the legislation of the Russian Federation provides such an opportunity by introducing benefits. The presence of children is a sign of one of the standard tax procedures carried out on the basis of a claim for a tax deduction for children.

The application of the child deduction is relevant if there is a child under the age of 17 in the family. It is allowed to extend the period up to 24 years in case of receiving education in an educational institution, regardless of the form of ownership, in a hospital.

The essence of the mechanism lies in the calculation of income tax (PIT) not from the amount of earnings of an individual, but its difference in relation to the deduction. The result is a reduction in taxation.

The essence of the mechanism lies in the calculation of income tax (PIT) not from the amount of earnings of an individual, but its difference in relation to the deduction. The result is a reduction in taxation.

The defining indicators of the tax procedure are:

The legislator does not set clear requirements for registration. An official document of special purpose has a specific addressee, usually the role goes to the employer. The procedure is acceptable when hiring a new employee. An annual application is not required. The head monitors the fact of the loss of the right to children's tax break by including this item in the obligations of the employee. The need to write a new paper is due to the birth of the following children.

The application form, the purpose of which is to reduce the income contribution, is characterized by general rules business in the field of application of details:

The application form, the purpose of which is to reduce the income contribution, is characterized by general rules business in the field of application of details:

The document is drawn up on behalf of the first person by any of the parents. Sample options are available in the form of handwritten and printed text.

The standard tax deduction is made from the calendar month in which the child was born. The content should not indicate the current period.

To provide tax deduction it is necessary not only to write an application, but also to attach a list of supporting documents for consideration, including:

To provide tax deduction it is necessary not only to write an application, but also to attach a list of supporting documents for consideration, including:

Employee tax office additionally may be required:

Consider the features of filling out application forms of a different nature.

The doubled amount is used if there is one parent (custodian, adoptive parent, guardian). Depending on the number of children, the monthly fee ranges from 2800 to 6000 rubles. rubles.

Providing deliberately false information about participation in the upbringing and maintenance of a minor entails illegal devastation of the budget and is prosecuted by the norms of criminal law.

The loneliness of a parent is determined by the death of the second, or by the presence of a mark on the absence of an entry in the birth document. The option of indicating information from words is quoted, while a certificate from the civil registration authorities (RAGS) is required.

The loneliness of a parent is determined by the death of the second, or by the presence of a mark on the absence of an entry in the birth document. The option of indicating information from words is quoted, while a certificate from the civil registration authorities (RAGS) is required.

Receipt property deduction possibly by a person who is not in an official registered relationship. The fact of adoption by a new spouse does not matter.

Divorce is not a determining factor in acquiring the status of a "single" educator.

To whom____________________________________

From whom (name, position _____________________

TIN __________________________________________

Address____________________________________

Statement

Receive double tax credit

I, (full name)____________________________, guided by p.p. 4 p. 1 art. 218 of the Tax Code of the Russian Federation, I ask you to provide a standard tax deduction for personal income tax on (full name) _____________________, _________ (date of birth).

I undertake to report the loss of the received right.

(Position) ____________ (full name)

(The date)__________________

According to the norms of the legislation in force in 2017, a double benefit is due to the father or mother of the child if one of the parties refuses to receive one. The assignment is made in case of proof of parental rights. The reduction in the amount of taxation is due to a certain list of requirements.

According to the norms of the legislation in force in 2017, a double benefit is due to the father or mother of the child if one of the parties refuses to receive one. The assignment is made in case of proof of parental rights. The reduction in the amount of taxation is due to a certain list of requirements.

Standard deductions are benefits guaranteed individuals income tax payers, subject to the required conditions (⊕ ). In particular, from the day the child is born, the person who maintains the newborn is entitled to a personal income tax deduction, the procedure for granting which is regulated by clause 4, clause 1, article 218 of the Tax Code of the Russian Federation. In the article we will talk about the application for a standard personal income tax deduction for children, we will give a sample of filling.

The right to a benefit is present if the age of the child does not exceed 17 years. Also, the right is extended until the 24th, if the adult is studying full-time in a foreign or domestic educational institution. It doesn't matter if the education is free or paid.

The essence of the benefit is the absence of taxation of the deduction, therefore, income tax to be withheld (13% of income) is calculated not from the amount accrued to the employee, but from the difference between income and deduction, which leads to a decrease tax burden on a physical person.

The amount of the deduction is influenced by the order in which the child appears, the presence of a disability, as well as the status of the person raising a minor. The actual values of the “children's” deduction for 2017 are shown in the table.

| To whom is it due | Who gets | |

| adoptive parents,parents and their spouses | Guardians (up to 14 years old), trustees (after 14 years old),adoptive parents, their spouses | |

| For a child born 1st or 2nd in the family | 1400 | 1400 |

| For a child born on the 3rd or subsequent | 3000 | 3000 |

| For a child with a confirmed disability 1 or 2 gr. | 12000 | 6000 |

In order for the employer to take into account the prescribed benefit when calculating personal income tax, it is necessary to inform him in writing, while confirming the declared right with documents. Documents are submitted to the tax agent. If there are several employers, then one of them is selected.

The set of mandatory documentation includes:

In addition to these documents, the applicant may be required to:

The document is drawn up in writing on paper or computer. Typewritten text is printed. The application must contain a standard set of details, the text is formulated in free form.

It is enough to submit an application once, it is not required to repeat its submission annually. The document is addressed to the employing organization, which acts as a tax agent. If the tax agent changes, the application is written again. This is possible when applying to another company or when reorganizing and changing the name of the current employer.

The reason for re-writing the application may be the birth of a new child.

The application form must contain:

The main attention should be paid to the text of the application, in which the employee needs to include the following information:

(click to enlarge)

You can use the benefit from the moment the child is born. You can submit documents to the employer for the deduction directly in the month when the birth is recorded. At the same time, the employer is obliged from this month to take into account the standard deduction when withholding income tax from payments to the employee.

If the employee provided documentation for the deduction later, then the employer is obliged to recalculate personal income tax from the month when the right to the benefit appeared.

If the newborn was born in February 2017, and the documents were submitted in May 2017, then the employer must recalculate income tax for the period from February to April. If the birthday fell on the previous year, then the recalculation is performed from the beginning of the year.

Question number 1. Where to write an application if an individual works part-time?

If the applicant for the deduction works simultaneously in several companies, then he can declare his right to any of them at will.

Question number 2. In what cases is an application for a deduction written again?

If the grounds for obtaining benefits from the employee do not change, then you do not need to re-write the application paper to the same tax agent. The application will need to be rewritten if:

Question number 3. Are there rights to a double deduction if the 2nd parent is deprived of parental rights?

Only the person on whose support the child is listed can receive the standard benefit. If one of the parents is deprived of parental rights, then according to the RF IC, he automatically loses the right to all benefits and benefits for people with children, but he is not exempt from the obligation to support the child and pay alimony. It turns out that the child is still listed on the content of the parent deprived of parental rights.

The standard "child" deduction is regulated tax code therefore, the provisions of the family code do not apply to the procedure for its provision.

A double deduction is due to the parent who has the status of "single", which is possible in the absence of the 2nd parent due to his death or disappearance, which must be confirmed by a court decision. The fact that one of the parents was deprived of the rights to the child does not give the second the status of "the only one."

Therefore the right to double size absent in this situation. A double deduction is possible if the parent who has lost parental rights voluntarily waives the right to the benefit and draws up a corresponding application.

For the 3rd and subsequent children, the amount of the deduction increases by more than 2 times. Therefore, it is necessary to correctly determine what kind of child is in the family in a row. It is necessary to take into account the order of birth, it does not matter how old the children born earlier, they should also be taken into account. Moreover, one must also take into account those children who have already died.

If there are 3 children in the family: the first is 32 years old, the second is 22 years old and he studies full-time at a university, the third is 10 years old, then parents are entitled to such deductions: