Tuition tax deductionand the deduction for treatment is combined into a group of deductions that are of a social nature and allow an individual to make a tax refund both for himself and for relatives. What amount can be returned using the tuition tax deduction and whose tuition it applies to, we will tell in this article.

Signed 2 p. 1 art. 219 of the Tax Code of the Russian Federation provides for the reimbursement of personal income tax when purchasing educational services due to the use of a tax deduction for training. The Tax Code of the Russian Federation allows this to be done in several ways:

The maximum possible amount that can be deducted when carrying out these actions should not exceed 120,000 rubles, i.e., up to 15,600 rubles can be reimbursed. tax (120,000 × 13%). When paying for the education of children, the maximum deduction limit for each child / ward is set at 50,000 rubles, and personal income tax from it will be 6,500 rubles. (50,000 × 13%).

IMPORTANT!The specified limit of 120,000 rubles. is determined taking into account all types of social deductions for individuals. For example, a citizen, having spent 80,000 rubles in 2017. for their education and 70,000 rubles. for treatment, will be able to return the tax only from 120,000 rubles. The balance in the amount of 30,000 rubles. (80,000 + 70,000 - 120,000) is not carried over to the next year.

For more information on the use of social security benefits, see .

Granting of a deduction is possible in the presence of the following set of documents:

In order to use the deduction during the year in which the expenses were actually made, these documents must be contacted by the IFTS, which will issue a notification of the right to deduction. And according to this notice, the tax will be returned at the place of work.

You can also get a refund directly from the IFTS. But this can only be done at the end of the year in which the right to deduction arose. In this case, a declaration in the form of 3-NDFL will be added to the above set of documents. From the moment of receipt of the documents, the IFTS conducts a desk audit within no more than 3 months, after which it makes a decision within 1 month and, if it is positive, refunds the tax that has been overpaid due to the application of the tax deduction for tuition. The period during which an individual can exercise his right to a deduction is limited to 3 years (letters of the Ministry of Finance of Russia dated November 17, 2011 No. 03-02-08 / 118, dated October 27, 2011 No. 03-04-05 / 7-815).

An individual can take advantage of the tuition tax deduction:

Is a social deduction possible if the study is remote, find out.

Example

In 2017, a citizen completed courses at a driving school, and also underwent advanced training.

In doing so, they incurred the following expenses:

A citizen has the right to claim 110,000 rubles for deduction. (50,000 + 60,000) if supporting documents are available.

At the same time, the main condition for obtaining a tax deduction for training is that the training organization has a license for educational activities.

How to issue tax deduction for education? The list of documents in this case is almost similar to the one indicated earlier:

For information on issuing a certificate in the form 2-NDFL, see the article .

There are some features of the emergence of the right to apply the tuition tax deduction when children receive education:

If these requirements are met in aggregate, then, by collecting required package documents and filling out the 3-NDFL declaration, an individual can count on a tax deduction for tuition.

At the same time, full-time education can be carried out by the following institutions:

Example

The citizen has two children under the age of 24. One child is engaged in painting, the other is studying at the evening department of the university.

During the year, the citizen made the following expenses:

A citizen can take advantage of a deduction of 50,000 rubles. only from the funds spent on drawing, because the form of education of the 2nd child is evening and compensation in this case is not provided.

The tax deduction for tuition is applied on the basis of the above-mentioned package of documents, and the degree of relationship in this case will be confirmed by the birth certificate of the child.

IMPORTANT!If an individual paid for the education of children from maternity capital, it will not be possible to return personal income tax.

For other deductions that a parent can use, see the article. .

An individual, as already noted, can take advantage of the application of the tuition tax deduction from the amounts directed to the education of a brother / sister.

This requires that:

Read about whether a deduction is possible for part-time education, read the material .

It should be noted that a brother / sister can be considered as such if there is at least one common parent.

The deduction is received provided that the taxpayer himself appears in the agreement with the educational institution and payment documents. To confirm the degree of relationship, photocopies of the birth certificates of the applicant and the student are submitted.

If a citizen has the right to guardianship, he can take advantage of the tax deduction for the education of a legal guardian.

Reimbursement is possible:

IMPORTANT!After the ward reaches the age of 18, the right to a tuition tax deduction from the person paying for his tuition also remains until the student reaches 24 years of age.

In order to receive a deduction in this situation, to binding documents sent to the Federal Tax Service, a document confirming guardianship is added.

Using the tax deduction for training on personal income tax, you can reimburse part of Money spent on education. But in order to do this, you need to make the right choice. educational institution: Lack of an educational license may prevent tax refunds.

Are you paying for your education or for your child's education? Take paid courses additional education Or driving school? Then you have the opportunity to receive a tax deduction for education. From this article you will find out who is granted a deduction, and what needs to be done to apply for it.

A tax deduction is an amount with which it is allowed not to pay personal income tax. As part of the deduction, you can return part of the taxes already paid or receive “tax holidays” for a certain period.

The basis for receiving a tuition deduction is the expenses incurred when paying for your own education or the education of your child, brother or sister.

You can get tax credits for own training, and for the study of their children, wards, brothers or sisters under the age of 24 years. If you are making a deduction for your education, it does not matter at what age you received it.

Other relatives cannot claim compensation. So, if a grandfather or grandmother paid for the education of their grandson, they will not be given a deduction. Also, the benefit is not provided if the child's education was paid for from maternity capital.

Both parents have the right to receive a deduction for the child's education, but the amount from which the tax can be returned should not exceed a total of 50,000 rubles. for each child for both parents.

It can be:

The license details are usually contained in the service agreement. If they are not listed there, a copy of the license itself will be required, which the institution must issue upon request. If you are planning to issue tax break for training, ask in advance if the organization or individual entrepreneur has the appropriate license.

The requirement for a license does not apply only to individual entrepreneurs who personally provide educational services, provided that information about their activities is reflected in the unified state register of individual entrepreneurs.

When making a deduction for your own education, it does not matter whether you studied full-time or part-time. But compensation for paying for the education of a child, brother or sister is due only on condition of full-time education.

Example 1. For studying at the institute, you pay 150,000 rubles annually. Your salary up to personal income tax deduction is 50,000 rubles, of which 6,500 rubles. the employer monthly transfers to the budget. Thus, per year you pay 78,000 rubles. income tax. Since the maximum deduction amount is 120,000 rubles. per year, you can return 13% of this amount, that is, 15,600 rubles. This amount is less than the personal income tax withheld from you, so you can return it in one payment.

Example 2. You take English courses and at the same time pay for your child's studies at the institute. The cost of the courses is 80,000 rubles. per year, the cost of studying at the institute is 100,000 rubles. in year. Your salary before personal income tax is 70,000 rubles, so the amount of personal income tax withheld from you for the year is 109,200 rubles. For a year, you can return 16,900 rubles: 10,400 rubles. for your own education (13% of 80,000 rubles) and 6,500 rubles. for the child's education (13% of 50,000 rubles). This amount is less than the maximum refundable amount, so you will also receive it in one payout.

Unused deduction balance for the next taxable period is not transferable, so it is better to pay for expensive tuition annually, and not in one payment for the entire period of study. So you can return tax every year from 120,000 rubles.

The deduction can be made for the last three years. At the same time, the date of payment is important for registration of the declaration, and not the date of commencement of training. So, if you paid for your studies at the end of 2017, and your studies began in January 2018, the deduction will be calculated from taxes for 2017.

Copies of documents must first be certified by a notary public or independently. With self-certification, on each page of the document, you must write “Copy is correct”, sign with a transcript and indicate the date.

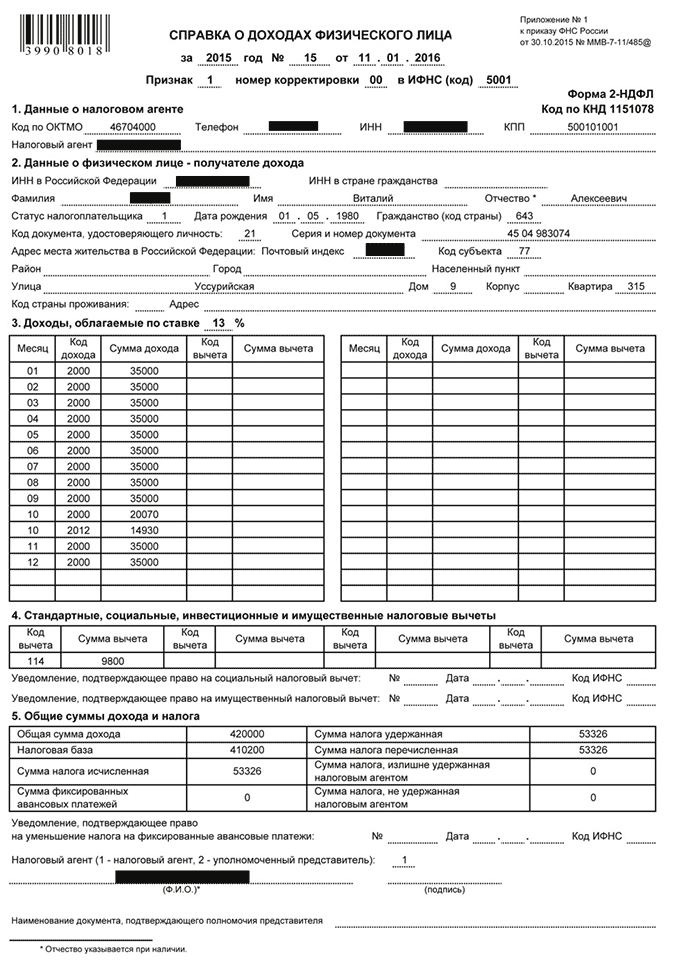

When submitting a request through the IFTS service, the 3-NDFL declaration can be filled out in in electronic format. The declaration will need to indicate passport data, information on income from 2-personal income tax and information on tuition payments. Other documents will need to be scanned and attached to the application. The average time for checking documents and transferring money is 30 days.

To do this, you will need to collect almost the same set of documents as when making a tax deduction. You will not need only a 2-NDFL certificate and an income declaration, but instead of an application for a deduction, you will need to fill out an application for issuing a notice (sample: (downloads: 19)).

Documents can be submitted directly to the IFTS branch at the place of registration and through the website www.nalog.ru. When applying in person to the tax office, you need to have a passport, copies and originals of all documents.

A month is allotted for verification of documents. If everything is done correctly, you will be issued a tax notice, which, along with your application (sample: (downloads: 11)) will need to be handed over to the employer. After that, personal income tax will no longer be deducted from your salary for a certain period.

You can apply for a tuition deduction an unlimited number of times. In this case, the deduction can be issued only for the last three years and for fixed amounts.

Have questions or need help with paperwork? Seek advice from experts who will advise you.

17.04.17 347 758 8

This year the tax will pay me 33 thousand rubles. This is my tuition tax deduction. Here's how I got it.

I entered the institute in 2012 for a paid department. At the same time, she got a job to pay for her studies on her own. At the beginning of 2017, I decided to get a tax deduction. Typically, the application for a tax deduction is submitted once a year. But I applied immediately for three years: 2014, 2015 and 2016.

To do this, I needed documents from the institute, a certificate from work, tax return and several statements. Most of the process could be done in my own accounting department, but since I quit, I had to go through all the steps myself.

Anastasia Manukhina

received a tuition tax credit

When you spend money on things that are useful to the state, the state returns part of this tax.

Non-working pensioners and unemployed students do not receive a salary and do not pay income tax, therefore they are not entitled to a deduction (Article 219 of the Tax Code). Can't get deduction individual entrepreneurs who have chosen the simplified taxation system, single tax on imputed income and the patent system. Also, the deduction is not provided for when paying for studies at the expense of maternity capital (subclause 2, clause 1, article 219 of the Tax Code).

You can get the deduction for yourself or for close relatives - children, sisters and brothers under the age of 24 - if you paid for their education. It is important that they study full-time, and not by correspondence. If you pay for yourself, then the form of training does not matter.

The deduction is received from the cost of studying at a university, kindergartens, schools, driving schools or centers for the study of foreign languages. The main thing is that the institution has a license to carry out educational activities. It doesn't matter if it's a public organization or a private one.

The maximum amount of expenses for which a social deduction will be given is 120,000 R per year and 50,000 R to pay for the education of children. The state will return 13% of this amount: up to 22,100 R in year. You can get two deductions per year if you paid for both yourself and your child. If you spend more on training, you will still get back only 22,100 R. Therefore, it is better to pay for expensive education in stages, and not immediately for several years.

Suppose a working student Anastasia receives 80,000 R per month. She earned 960,000 rubles a year. Of this amount, she received 835,200 R. 13% of income tax was paid for by the employer - 124,800 R.

Nastya spent 40,000 on training R, by 20 000 R per semester. She applied for a tax deduction.

After submitting the application, the tax authority will deduct education expenses from Nastya's income for the year and recalculate her personal income tax:

(960,000 − 40,000) × 0.13 = 119,600 R

It turns out that Anastasia had to pay 119,600 R, but actually paid 124,800 R. The tax will return the overpayment to her:

124 800 − 119 600 = 5200 R

The tax deduction can be received for the past three years. In 2017, you can get a deduction for 2016, 2015 and 2014.

When receiving a deduction, the date of payment for the semester is important, and not the date it starts. For example, you paid for the semester in December 2015, and it began in January 2016. This check is attached to the application for 2015, not for 2016.

The easiest way to submit documents at work: you will only need to bring a notification from the tax office about the right to a deduction, the rest will be done for you in the accounting department (clause 2 of article 219 of the Tax Code of the Russian Federation). But this option did not suit me, because I had already quit.

If you have a personal account on the website of the tax service - apply there. To gain access to the office, you will have to contact the nearest tax office. The username and password from the State Services website are also suitable.

I did not have access, and I gave the documents personally.

Documents from the educational institution. You will need a copy of the agreement and a certified copy of the university license, as well as payment documents: checks, receipts, payment orders.

The agreement with the educational institution can be submitted to the tax office in the original. A certified copy is required for a university license. You can certify a copy with a notary or in the educational institution itself.

You will also need original pay stubs. If you have lost a check, it can be restored in the accounting department of the institute or in the bank (if the payment was made by bank transfer). I lost one check. Restoring the check cost me 160 R and two hours of wasted time: I had to go to the institute and write an application for a copy of the payment document.

If the tuition fee was increased, then you must provide documents confirming the increase.

It is issued in the accounting department of the company where you work or worked. If in three years you have changed several jobs, you will have to go and collect documents from everywhere. The certificate must indicate how much you received and how much income tax was paid for you.

Before you go to the accounting department for help, call and ask if it is ready. I arrived a couple of times at the appointed time, and then waited, because the accounting department did not have time to complete it.

To fill out the declaration, you will need passport data, checks from the cash desk of the educational institution to calculate the amount of the tax deduction, and information from the 2-NDFL certificate: employer data, codes and amounts of income.

Tax refund application. Fill it out by hand or electronically. In the application, indicate the details of the bank and the number of your account, to which the state will transfer money to you.

In the application, you can immediately indicate total amount deductions for several years.

Identity documents. You need a passport and a copy. If you paid for the education of your children, brother or sister, you need to bring documents confirming the relationship (for example, a birth certificate) with you.

I collected all the documents and went to the tax office. I put a whole day on this adventure, but in reality everything turned out quickly.

I took the number electronic queue, and I was invited to two windows. In the first, I handed over all the documents except for the application. Submitted the application in the second window. I got it all done in half an hour.

Tax checks documents up to three months. The inspector can find errors and refuse a tax deduction - then you will have to submit documents again. In this case, when filling out, you must indicate that you are submitting a corrective declaration.

Everything was in order with my documents. Within a month, I received my tax deduction in my bank account.

Applying the tuition deduction reduces tax base on personal income tax persons with taxable income.

You can use the benefit when applying to the Federal Tax Service with an application, a 3-NDFL declaration and documents confirming the right.

The tax refund is carried out by the Inspectorate or the employer.

The social deduction allows you to make a refund of part of the expenses incurred when paying for your own education or close relatives.

The deduction in the amount of expenses incurred is applied to the tax base for personal income tax - income received in the calendar period. The refund is subject to the withholding tax limit and the deduction limit.

Peculiarities tax deduction:

Benefit amount depends on the category of persons whose tuition fees are paid by the taxpayer. The procedure for granting a deduction, the categories of persons whose education is privileged, the workflow is established by Art. 219 of the Tax Code of the Russian Federation. The legislation does not establish a restriction on educational institutions. It is allowed to claim deductions for training received in public or commercial institutions.

There is an opportunity to receive benefits compliance with the conditions:

Tax refunds are not made on the deduction of expenses reimbursed by the enterprise (employer of the taxpayer), social fund, maternity capital or other structure. The deduction is granted only to the individual who incurred the expenses.

Tax refund produced at cost incurred:

The refund of previously paid tax is made for 3 years prior to applying to the IFTS.

For example, if an appeal to the IFTS is made in 2019, a deduction can be claimed for 2016-2018 years of study. The declaration is submitted within the calendar year following the year in which the expenses were incurred. statute of limitations established in the Civil Code of the Russian Federation and is equal to 3 years. After the period limitation period deduction is not provided.

For example, if an appeal to the IFTS is made in 2019, a deduction can be claimed for 2016-2018 years of study. The declaration is submitted within the calendar year following the year in which the expenses were incurred. statute of limitations established in the Civil Code of the Russian Federation and is equal to 3 years. After the period limitation period deduction is not provided.

To get the deduction, the training time does not matter. The fact that the student is on academic leave does not affect the tax refund. When determining the limitation period, the calculation of the period for claiming a deduction takes into account the year the payment was made. As payment documents standard forms are accepted - an extract for a transfer from a current account, a receipt for a cash contribution, and others.

The amount of the social deduction provided for tuition is marginal constraint established in Art. 219 of the Tax Code of the Russian Federation. The taxpayer's own tuition fee is limited to 120,000 rubles annually. The amount of the deduction for the expenses of training relatives is set at 50,000 rubles, provided for each of the persons.

The amount of the social deduction provided for tuition is marginal constraint established in Art. 219 of the Tax Code of the Russian Federation. The taxpayer's own tuition fee is limited to 120,000 rubles annually. The amount of the deduction for the expenses of training relatives is set at 50,000 rubles, provided for each of the persons.

The peculiarity of the provision of social deduction is the presence general restriction for all types of deductions. It is possible to apply the full amount of the benefit in the amount of 120,000 rubles spent on education only if there are no other declared social category deductions - treatment, purchase of medicines, participation in non-state pension insurance. If there are several types of deductions in tax year the individual has the right to choose.

Consider the case of a tax refund when paying for children's education.

Citizen Konev A.A. has income from normal look activities as an employee. In 2018, Konev A.A. received an income of 300,000 rubles. The person has three children and paid for their education in 2018 in the amount of (50,000 + 40,000 + 40,000) = 130,000 rubles.

Suppose the employee did not use the right to standard deduction and applies only social deduction. The amount of tax payable before the exemption is applied: 300,000 * 13% = 39,000 rubles. After checking the documents by the Federal Tax Service Inspectorate, the citizen was granted a deduction in the full amount of paid education for children. The amount of tax payable by an employee in 2018 decreased and amounted to (300,000 - 130,000) * 13% = 22,100 rubles. Citizen Konev A.A. has the right to return the tax in the amount of 16,900 rubles.

To receive a benefit in the form of a deduction with a subsequent refund of overpaid tax, you will need submit a 3-NDFL declaration with supporting documents attached. Forms confirm the fact of education, payment, relationship and the availability of taxable income. Submitted as a separate document statement for a refund.

Part applications when receiving a deduction for the education of the taxpayer, includes:

The list of documents can be expanded at the discretion of the territorial Inspectorate of the Federal Tax Service. So, some authorities oblige to provide an act of acceptance and transfer of services, additional annual agreements to the contract and other forms. The main list of documents of the Inspectorate is published on the official website or information stands. In some cases, the submission of clarifying documents may be requested by the inspector who checks the right to the benefit in camera.

When claiming a deduction for teaching relatives in addition to the main list of securities, the following are submitted:

If a non-payer was accidentally indicated in the payment documents for the education of relatives, you will need to provide a notarized power of attorney for the right to deposit a specific amount on the specified date under the contract. The opinions of the IFTS on the issue of payment details differ, which creates the prerequisites for refusal when making amounts by third parties. In the case of issuing a payment document for the spouse of the applicant for benefits, a marriage certificate must be attached.

Tax control individuals and the provision of benefits is carried out by the territorial IFTS.

To receive a deduction would need:

Submission of documents for benefits is carried out in person, by mail or through a proxy. The taxpayer can use the right to submit documents through a personal account opened on the official website of the Inspectorate. Usage personal account allows you to save time and provides an opportunity to track the end of the check.

Reimbursement of overpaid taxes in non-cash form.

After graduation desk audit the amount of the overpayment is recorded on the personal account of the taxpayer, which has a breakdown by type of tax. The transfer of funds to the current account of a person is carried out on the basis of an application and according to the data provided in the document. If you do not have an account, you will need to open it at any branch of the bank.

The application is drawn up by a person in writing according to the model provided by the Federal Tax Service.

Applies drafting form statements:

The document is signed by the taxpayer personally with the decoding of the full name and date of the application. It is possible to apply for the transfer of the amount at a later time. You can receive the due amount within 3 years from the date of the end of the desk audit. After the expiration of the period, the amount remains on the personal account of the taxpayer, but it is not possible to use it (offset, return).

The deduction for the education of the child is provided only for full-time payment, which implies attendance at the institution of permanent and regular classes. In full-time or evening form, studies are carried out in an irregular mode and are used in universities or institutions of a secondary special profile.

The deduction for the education of the child is provided only for full-time payment, which implies attendance at the institution of permanent and regular classes. In full-time or evening form, studies are carried out in an irregular mode and are used in universities or institutions of a secondary special profile.

Courses, studies at a driving school, sections or hobby groups cannot have options for providing in the evening or by correspondence. Training is conducted on a regular basis, which makes it possible to classify training as full-time. To confirm the fact of regular study, you must provide a certificate or have a footnote in the contract.

The expenses claimed for deduction include only payments for tuition. There is no concession on associated amounts. For example, if the cost of a foreign language course includes lunch, the amount should be excluded from the cost. To obtain the exact amount of non-training expenses, you will need to additionally provide an estimate of the costs of the institution for a particular student.

For information on this type of social tax deduction, see the following video:

Last updated June 2019

In order to apply for a tax deduction for education, you will need the following documents and information:

for teaching children

When filing a tax return for brother/sister additionally provided:

When applying for a tax deduction for studying abroad, the following are additionally provided:

It should be noted that in order to avoid delays and refusals, contact tax service follows from the most complete package of documents.

The "Tax Refund" service will help you quickly and easily prepare a 3-personal income tax return and an application for a tax refund by answering simple questions. In addition, he will also provide you detailed instructions for submitting documents to tax authorities, and in case of any questions when working with the service, professional lawyers will be happy to advise you.

By law, all copies of documents must be notarized or independently certified by the taxpayer.

In order to certify yourself, you must sign every page(not each document) copies as follows: "Copy is correct" Your signature / Signature transcript / Date. In this case, notarization is not required.