Briefly: Gross profit is an indicator of the profitability of the enterprise. The indicator is calculated as the difference between revenue and cost.

There is no standard, the higher the value, the greater the profitability of the company.

The effectiveness of any commercial activities determines the size of its profit or the difference between income and expenses. This indicator cannot be negative, otherwise it is called a loss. Depending on the composition of costs and the peculiarities of calculations, profit can be economic, accounting, balance sheet, gross, net, operating, marginal, target, lost, normal, consolidating, etc. In total, there are more than 20 types of profit.

Gross profit (EBIT, VP) is the difference between revenue and the cost of products / work / services. Expressed in monetary terms.

In simple words: this is the profit received from the sale of goods/services, excluding some types of costs (taxes, excises) that are not associated with the costs of manufacturing and selling goods/services.

You can learn about the features of calculating gross profit from the video:

To calculate the VP, it is customary to use the following formula:

VP \u003d B - C, where:

For trade organizations, the option is more suitable:

VP \u003d VD - C, where:

Revenue - money received for the sale of services / work / goods.

This is the amount that the buyer leaves in the store and thereby pays for the cost of the product itself, the cost of pre-sale preparation, the amount of taxes (VAT, excises), service. Revenue includes only those receipts that arose as a result of the conduct of the main activity. it cash flow that passes through the organization.

Gross income - the amount of proceeds from the sale of goods / services, fixed assets, shares, intangible assets, rights intellectual property, is calculated by the formula:

VD \u003d (T x SPN) / 100, where:

Reference! The main difference between gross income and revenue is that gross income includes turnover from other activities.

Cost - the cost of production and sales of products. It includes:

The cost does not include administrative and commercial expenses.

Reference! Depreciation of fixed assets - a gradual write-off of the cost of purchasing fixed assets (buildings, structures, equipment, patents, etc.) in subsequent periods after the acquisition.

In other words, if a company bought a machine for 10 million rubles, then it does not reflect the entire cost in the balance sheet, otherwise there will be a loss, but writes off the purchase amount over several years in small shares.

EBIT- important indicator financial economic activity any enterprise. On the basis of VP, all other types of profits are already considered, including net profit.

The size of the VP is influenced by external and internal factors. Of decisive importance is the scope and specificity of the company's activities, its location, the size of the enterprise, the reach of the audience, and the demand for the product.

Internal factors depend on the actions taken by the organization itself, external - on other independent aspects of the market economy.

All of them affect the cost price and sales volumes.

Rice. 1. Gross profit growth

A special place is occupied by unsold goods. They are in warehouses and cause losses. They may be unsold different reasons: a drop in demand, there was a large supply, the human factor (not put up for sale), seasonality, a change in fashion trends. In order to sell such goods faster, marketing tricks are used: they assign discounts, arrange promotions. You can return the goods to the supplier if they were taken for sale.

VP includes all expenses that are related to the main activities of the company. Therefore, the funds received from the sale of products / services must be correctly distributed so as not to miss a single item of expenditure.

Costs covered by VP:

In the final balance, net profit is obtained, from which the income of the enterprise is formed. It is already directed to reserve funds, to staff training, expansion, diversification, and development of the company.

For analysis, balance sheet data for the year, quarter or month is used. You can download an example calculation in Excel.

|

Cost price |

Gross profit |

Gross profit 2017 to 2016 |

||||||

|---|---|---|---|---|---|---|---|---|

|

Deviation |

||||||||

|

September |

||||||||

The table shows that the GDP indicator for each month of 2017 is greater than it was in 2016.

This means that the company is doing better, despite the seasonal drawdown from March to June. Growth for the year amounted to 253,600 thousand rubles. or 132.8%.

Rice. 2. VP in dynamics

Important! When calculating revenue and cost, you need to keep in mind the real level of inflation, since it directly affects the rise in prices.

EBIT does not have any normative value, since the greater the gross profit, the better for the enterprise. It is necessary to compare the value of the indicator in dynamics and as a percentage of costs and net profit.

No questions have been asked for the material yet, you have the opportunity to be the first to do so

The difference between the costs of society and the enterprise and, accordingly, between the price at which the enterprise sells products and its cost forms net income enterprises. The main form of net income is profit. Profit reflects the results of economic activity, that is, the productivity of living and materialized labor, therefore it is an important characteristic of the efficiency of the enterprise. Net income means that it is a part of the company's income.

By labor theory cost gross income- this is the proceeds from the sale of products without material costs, the monetary form of the net production of the enterprise.

C+ V+m

FROM – material costs;

V- the cost of wages;

m- net income (surplus value)

c+v- production costs.

v+m- newly created value (gross income of the enterprise).

The mass of profit and gross income characterize the size of production efficiency: production volume, quality, use of resources. To determine the profitability of the enterprise, the profit is compared with the advanced capital.

Rate of return

P \u003d p / (c + v) * 100%

where p is profit.

Gross income is the total amount of income from all activities of the enterprise. The amount of expenses of the enterprise forms gross costs.

Profit is the main source of development of the enterprise, scientific and technical improvement of its material and technical base, all forms of investment, payment of taxes.

The main part in the total profit of the enterprise - sales profit(Pr) Pr = f (output, cost, price)

Profit from other sales (Ppr)- excess of income from non-industrial production (works, services) released to the side, from the sale of materials, means of labor, intangible assets (inventions, trademarks, industrial designs, know-how, software, data banks) over expenses.

Profit from non-operating operations (Pvr)- the difference between income and expenses for these operations. These are operations that are not related to the sale of products: share in joint ventures, placement on deposit accounts in banks free funds, receipt of fines, debts, penalties.

Balance profit:

Pb \u003d Pr + Ppr + Pvr

The balance sheet profit after taxes is called net profit. It goes to the social and economic goals of the enterprise: the development of production, in reserve fund, to the social and cultural sphere, to charitable foundations.

Gross income(gross income) is an economic indicator characterizing the value newly created by labor.

Gross income expresses the total annual income of an enterprise, organization received as a result of the production and sale of products, goods and services; is defined as the difference between revenue and material costs for the production and marketing of products. Includes funds for wages and profits.

The value of gross income is greatly influenced by price changes. Therefore, gross income is determined not only in current prices, but also in comparable prices. They evaluate both sales revenue and material costs. The gross income indicator is used in planning and evaluating the performance of trade, procurement, supply, and marketing organizations.

Gross income is the income that the company receives from its main activities. In many countries, the term gross income is synonymous with turnover. For some companies, the source of gross income may be interest, dividends or royalties paid to them by other companies. The amount of gross income may refer to all gross income or gross income for a certain period of time in a certain currency, for example, “Last year, company “X” received a gross income of 1 million dollars. USA".

For non-profit organizations, the annual gross income may be referred to as gross funding income. This funding includes donations from individuals or companies, funding from government agencies, income from activities permitted by the charter non-profit organization, income from shares associated with the attraction of donations, membership fees or income from the placement of authorized capital funds.

Thus, gross income is the total income of an enterprise (company) from all types of economic activities and business transactions before payment of tax payments from it included in the price of products (value added tax, excise duty, customs duties and duties). The basis of the gross income of enterprises is the proceeds from the sale of products. Gross income also includes receipts from the sale of capital property, securities, patents and licenses, as well as received dividends and interest on debts, rental payments on leased property.

Incomes of the enterprise by spheres of education are divided into operating (main) and non-operating.

According to the State Standard of the Russian Federation GOST R 51303-99 “Trade. Terms and definitions” gross income of trade is an indicator that characterizes the financial result of trading activities. It is defined as the excess of revenue from the sale of goods over the cost of their acquisition for a certain period of time. Naturally, as a "certain period of time" in accounting is understood reporting period. Therefore, in order to determine the gross income of a trade organization for a certain period of time, we need to know the amount of proceeds from the sale of goods for this period and the amount of costs associated with the acquisition of goods.

The issues of determining, accounting and reflecting in the accounting of the gross income of the enterprise are considered in the "Methodological recommendations for accounting and registration of operations for the receipt, storage and release of goods in trade organizations", approved by the letter of Roskomtorg dated July 10, 1996 No. 1-794 / 32-5 , namely in paragraph 12 "Accounting for gross income from the sale of goods." As costs associated with the acquisition of goods, this document recognizes their purchase price, defining gross income as "... the difference between the sales proceeds (sales value of goods sold) and the purchase value of goods sold." Therefore, the concept of gross income is equated with the concept of realized trade markup (trade markup relating to goods sold over a certain period).

The definition of gross income depends on whether the goods in the trade organization are accounted for at purchase or sale prices.

If the accounting of goods at a trade enterprise is carried out at purchase prices (practice shows that this method is currently the most common), then the gross income of the enterprise will be reflected as credit balance account 90 “Sales” as a result of entries for accounting for recognized revenue and written off cost of goods:

Debit account 62 "Settlements with buyers and customers",

Sub-account credit 90.1 "Revenue" - recognized revenue from the sale of goods;

Debit sub-account 90.2 "Cost of sales",

Account credit 41 "Goods" - written off the cost of goods sold.

The financial result of trading activities (i.e., determining profit or loss from the sale of goods) will be determined on the same account, taking into account the total balance of sub-account 90.2 "Cost of sales" and sub-accounts intended for accounting for taxes that are integral part commodity prices (VAT, excises, export duties). These are sub-accounts 90.3, 90.4 and 90.5, respectively. These sub-accounts are opened in cases where the organization is a payer of these types of taxes and fees.

Profit or loss from the sale of goods at the end of the reporting period is reflected in sub-account 90.9 "Profit / loss from sales" and written off to account 99 "Profit and loss":

Debit account 90.9 "Profit / loss from sales",

Credit of account 99 Profits and losses ”- profit from sales is reflected;

Debit account 99 "Profit and loss",

Credit of account 90.9 "Profit / loss on sales" - loss on sales is reflected.

Suppose that a trade organization sold a batch of goods in the amount of 118,00 rubles during the reporting period, including 18% VAT - 18,000 rubles. The cost of goods amounted to 80,000 rubles. The item has been paid in full. Then the following entries will be made in accounting: Debit account 62 “Settlements with buyers and customers”, Credit account 90.1 “Revenue” - 118,000 rubles. - reflected the proceeds from the sale; Debit account 90.2 "Cost of sales", Credit account 41 "Goods" - 80,000 rubles. - the cost of goods sold was written off; Debit account 90.3 "Value added tax", Credit account 68 "Calculations on taxes and fees" - 18,000 rubles. - VAT charged; Debit account 51 "Settlement accounts", Credit account 62 "Settlements with buyers and customers" - 118,000 rubles. - payment received from the buyer. At the end of the reporting period, an entry will be made: Debit account 91.9 “Balance of other income and expenses”, Credit account 99 “Profit and loss” - 20,000 rubles. - reflects the profit of the reporting period. Thus, the profit from the sale of goods will be 118,000 rubles. - 80,000 rubles. -18 000 rub. = 20,000 rubles. And the gross income, according to the definition, will be 118,000 rubles. - 80,000 rubles = = 38,000 rubles.

If a commercial enterprise keeps records of goods at selling prices, the gross income is determined by the calculation method. The main methods are calculations:

1) by total turnover;

2) according to the range of goods turnover;

3) by average percentage;

4) according to the assortment of the rest of the goods.

The first method of calculation (according to total turnover) is used if the same percentage of the surcharge is applied to all types of goods. If this percentage has changed over time, then the calculation should be carried out for each period in which the percentage of the premium did not change. For this calculation method, the formula is used:

The volume of total turnover x estimated trade markup /100.

In turn, the estimated allowance is determined by the formula:

Percent Trade Markup / (100 + Percent Trade Markup).

The calculation of gross income for the range of goods turnover is used if different amounts of the trade allowance are applied to different groups of goods. In this case, it is obligatory to keep records of the turnover by groups of goods with the same markup. To calculate the turnover for each group of goods, they are multiplied by the estimated trade markup for this group. The resulting products are summed up and the sum is divided by 100.

The calculation of gross income by average percentage is the simplest and can be applied in any organization that keeps records at sales prices. For this calculation, the total turnover is multiplied by the average percentage of gross income, and divided by 100. The average percentage of gross income, in turn, is calculated as follows: – Trade markup for retired goods) / (Turnover + Balance of goods at the end of the reporting period) X 100.

The calculation of gross income for the assortment of the balance of goods is determined as follows. Trade allowances for the balance of goods at the beginning of the reporting period and those received for the reporting period are summed up, trade allowances for retired goods and for the balance of goods at the end of the reporting period are deducted from this amount.

Every business endeavors to maximize revenue. When developing a performance improvement strategy, an organization should consider financial indicators. One of the most important characteristics in this area is gross profit.

The indicator characterizes the financial result from the position of taking into account only production costs.

A feature of this type of profit is the inclusion of administrative and commercial expenses in the amount.

In other words, the gross profit, among other things, contains the salaries of the PMA, the costs of concluding agreements and contracts, and other institutional costs.

The indicator is found as the difference between revenue and technological cost, which, in turn, consists of the cost of materials, wages of workers and workshop costs.

Each group of indicators is subdivided into narrower ones. It must be understood that the income of managers directly related to the process of manufacturing products is taken into account in the technological cost.

The indicator is based on the company's data for the period. Generally, gross profit is calculated once a year.

Two indicators are used in the calculation - revenue and technological cost for the entire volume of production (excluding commercial and administrative expenses).

AT general view gross profit can be found using the following formula:

GP = TR – TC tech, where

GP (gross profit) - gross profit, rub.;

TR (total revenue) – revenue, rub.;

TC tech (total cost) - technological cost, rub.

The data for calculating gross profit are in the form financial statements titled "Statement of Financial Performance". In accordance with the provisions of the report, the formula looks like this:

Page 2100 = page 2110 – page 2120, where

line 2100 - gross profit, rub.;

line 2110 - revenue, rubles;

line 2120 - technological cost, rub.

Ekran LLC is engaged in the production of drills for milling machines. Financial statements for the last 2 years contains the following data:

Then the gross profit for 2013 and 2014, respectively, is:

GP 2013 = TR - TC tech = 120,000 - 40,000 = 80,000 rubles

GP 2014 = TR - TC tech = 180,000 - 60,000 = 120,000 rubles

Video - report "gross profit" in the program 1C: Trade Management:

The direct dependence of the indicator on the amount of revenue and technological cost is obvious. The higher the sales volumes at constant unit costs, the greater the gross profit.

The calculation of gross profit is especially relevant with a relatively small share of management and commercial expenses. If they do not exceed 5% of full cost, then it is advisable to use the considered indicator for short-term and medium-term planning.

In the case of long-term planning, it is rational to calculate other types of profit. For example, margin.

The indicator can also be used in budgeting and flow Money for the next period.

It is worth remembering that this species profit is close to production and does not reflect, for example, advertising costs. Therefore, for the final budget, the analysis of one gross profit will not be enough.

In some sources, you can see that these two types of profits are identical. This is not always the case.

The fundamental difference is that gross profit represents the difference between revenue and the totality of variables, as well as parts of fixed costs.

Marginal profit is revenue minus only variable costs.

Often the company incurs fixed costs, so the gross profit will be less than the marginal profit. To fixed costs include rent, depreciation and utility bills.

Gross profit is important for manufacturing enterprise, because it allows you to evaluate the magnitude and significance of the technological cost. The indicator must be taken into account when planning for a period of 1-3 years.

Video - what is the difference between profit and gross income:

Gross profit is a key criterion for the activity of an enterprise, characterizing its efficiency. The calculation of this indicator makes it possible to identify promising directions the work of the organization, distribute financial assets into more profitable niches, give an answer to the question: .

Profit maximization is the goal of any commercial enterprise. Gross profit is the amount of money that is received from the sale of a particular product or service, minus expenses.

In order for a company to get it, it is necessary that the goods or services sold are in demand. Pricing policy largely depends on the cost of production, production costs are also important. The indicator makes it possible to determine how effectively material and intangible assets.

Gross profit is the difference between total revenue and expenses. It can be calculated by subtracting from the proceeds from the sale of products (services) the costs of production, purchase, and organizational moments. Revenue is all the money received from the sale. The cost price includes all existing costs for the production of goods. If the company is engaged in the provision of services, the calculation takes into account all the costs associated with their provision.

Gross profit can be determined at any time for any period of time, it all depends on the management accounting of the company, on whether. As a rule, it is calculated at the end of the month, quarter and year.

To determine gross profit, two indicators are used - revenue and technological cost for the entire volume of production (excluding commercial and administrative costs). There are other types of calculation. Let's consider the main ones.

This method is used by retail companies if the same markup is set for all products sold by the company. In some cases, it is more convenient to calculate this indicator, starting from the value of the company's turnover. Turnover is the amount of revenue, including value added tax. For this you need:

You can also apply the following formula:

Often, for calculation, they take data in the balance sheet of the enterprise and the report on financial activities companies. This method is relevant for enterprises operating on. In this case, the calculation algorithm looks like this:

P.2100 = p.2110 - p. 2120, where

Example 1 (by balance):

JSC "Intensiv" is engaged in the production and sale of agricultural machinery. Its financial results for last years(according to the data on the financial activity of the enterprise):

Calculation of the gross profit of JSC "Intensiv":

As can be seen from the calculations, over the year the company increased its income by 40 thousand rubles, so in 2017 it should continue to work according to the chosen strategy, while looking for new ways of development.

Example 2 (for turnover):

In the Yagodka grocery store, a 35% mark-up is set for all products. For the year, the total revenue amounted to 150,000 rubles (including VAT).

The estimated premium will be: P(supercharge) \u003d 35%: (100% + 35%) \u003d 0.26. In this case, the amount of the implemented overlay will be: 0.26 * 150,000 rubles. = 39,000 rubles.

Gross profit is also determined when budgeting, when distributing monetary assets for the next quarter or year.

note: gross profit depends on the production process and does not always reflect the real picture of the efficiency of the enterprise. For example, it does not take into account the costs of marketing, logistics. Therefore, for the preparation of the final budget, the calculation of one such indicator will not be enough.

Depending on the field of activity of the enterprise, the cost and income items that are included in the cost and revenue may differ. This should be taken into account when calculating.

The revenue of a manufacturing enterprise depends on:

The cost of such companies includes:

The revenue of companies that sell goods depends on:

The cost of trading companies consists of the following items:

All of the above expenses and incomes must be taken into account when calculating economic indicators.

Often the product is written off as a minus. This means that according to the documents, the products are not in stock, but they are still being sold. With a surplus of goods or regrading, you need to take an inventory of the warehouse and capitalize the surplus. This is important to do before the product is sold.

Gross profit is often confused with marginal profit. Some sources even today identify these concepts. In fact, the difference is that gross profit is the difference between revenue and variable and fixed costs. Marginal takes into account only variable costs.

In practice, the company often incurs fixed costs, so gross income is less than marginal income. Fixed costs include rent, utilities, depreciation.

Save the article in 2 clicks:

Any commercial company, when making important decisions, is repelled by profitability indicators. Gross profit is indicated in the balance sheet, it is important for the production sector, as it makes it possible to analyze the technological cost. The indicator is taken into account when planning for 1-3 years, to build a strategy and tactics of action.

In contact with

The economic activity of enterprises is based on making a profit. It becomes an indicator of the quality of work of all its employees. Gross profit characterizes the effectiveness of using all the capabilities of the organization.

For some types of enterprises, there are differences in the definition of gross profit. Not everyone can benefit from this economic indicator.

The performance of different companies is compared in terms of EP. Additionally, gross profit is calculated for other types of work within the organization in order to analyze the effectiveness of the product release.

Gross profit is the amount of value gained from various types of work minus the associated costs. For example, the main profit comes from the sale of a product, and its initial cost will be a waste. The difference between the two values will be the gross profit for the main type of work.

Similarly determine the gross profit from all possible types of work. It is interesting that in trading it will be a quantitative difference between the sale and the initial price. For production, gross profit is found using a more complex formula, since the cost price includes many components that are subject to certain rules.

Trade is understood as making profit through mediation between the end consumer and the producer. The organization must buy products from the manufacturer at a price close to the cost, and then send it to outlet for sale to buyers at a premium.

VP - the difference between the amount of purchase of goods and its implementation. The difference between gross and net profit is that the first is equal to the income received before mandatory deductions, deductions. Gross profit does not include spending on taxes and unavoidable payments.

Consider the concept, features of gross profit for various cases:

Gross profit will be the main measure of profitability or revenue. It is often used to analyze the performance of an enterprise.

To correctly determine the VP, it is necessary to take into account all expenses without exception, including the cost of goods. Under the cost understand the set of expenses in monetary terms for the manufacture of goods.

There are two types of reasons that affect gross profit. The first includes internal factors that depend on the management of the enterprise:

External consider those that cannot be influenced:

Reasons that can be influenced are considered more significant. The need for goods depends on them.

Consider the organization of pricing policy. In a crisis, the management of the organization must competently approach pricing. We need the right approach to consumers in order to use a minimum of funds to attract them.

However, a constant price reduction can increase turnover, but does not always ensure the financial well-being of the organization. It is better to have a good volume at a reasonable price than to sell more at a lower price.

When analyzing profitability, knowing the exact consumer demand, it is permissible to expand the output of demanded products by reducing or removing another category of products. This will help you make a profit from in-demand goods and reduce the cost of unclaimed ones.

There are several types of gross profit, and, accordingly, the formulas for calculating them are different. The classic formula for calculating VP is quite simple and understandable - the difference between the net profit from sales and the initial price of the goods (cost price). Unlike net income, it does not contain variable or operating expenses, taxes.

VP \u003d P - S

VP- gross profit;

P- profit from the sale of products;

FROM- the cost of production.

In order to optimize the value of VP, they begin to work with cost items included in the initial cost, and cover variables that were not previously included in the calculation.

Focusing on the costs of production, the sale of goods, you can accurately determine the gross profit in a certain period.

Organizations whose accounting is based on sales prices calculate the financial result in accounting by a different method. Since accounting is based on the price paid by the consumer, the actual write-off from account 90 is based on the price of the sale price. In other words, the proceeds from the buyer is equal to the amount that is debited from the loan account. 41-2 to debit account. 90 for the sub-account "Cost". For finding financial result write off not the selling price, but the difference between the retail and purchased prices - reverse the trade margin on the account. 42. This difference will be gross income or realized overlay.

After the third-party trading margin on the account. 90 forms the credit balance, which will be the gross income from the sale of products.

It is permissible to use by retail organizations if all goods sell at one trade margin as a percentage.

The turnover is considered to be the total revenue with VAT, which is stated in clause 2.2.3 methodological recommendations №1-794/32-5.

PD for turnover:

VD \u003d T * PH

T- the total amount of turnover, for wholesale organizations use wholesale turnover with warehouse and transit;

RN- estimated markup:

PH \u003d TH / (100% + TH)

TN- established trade markup.

Consider an example. In the store for the entire range of trade margin 30%. Revenue for the period under review is 170 thousand, including VAT.

pH = 30%/(100%+30%) = 0.23

VD \u003d 170,000 * 0.23 \u003d 39,100 rubles.

If the trade margin has changed in the reporting period, then the use of the method is possible, but the PD is determined and calculated separately for different periods.

The calculation method is used when setting a different trade margin for different types of goods.

Gross income is calculated:

VD = (Т1*РН1+…+ Тn*РНn)/100

The turnover (T) and the estimated margin (PH) are taken separately by groups.

Example. In the store I sell dairy products with a markup of 25%, and bakery products - 20%. Revenue for the period in the dairy department is 120 thousand rubles, and in the bread department - 90 thousand rubles.

Estimated markup in the dairy department РН = 25*(100-25) = 0.2. The size of the implemented overlays of VD = 120,000 * 0.2 = 24,000 rubles.

Estimated markup in the bread department РН = 20*(100-20) = 0.17. The size of the implemented overlays of VD = 90,000 * 0.17 = 15,300 rubles.

The total amount of gross income: IA \u003d 24,000 + 15,300 \u003d 39,300 rubles.

When changing the margin, the calculation is carried out separately for groups.

The most common method in retail. VD is determined by:

VD \u003d (T * P) / 100

T- turnover

P- average percentage of VD:

P \u003d (Nn + Rp-Nv) / (T + Ok) * 100%

Hn- margin on the remaining goods at the beginning of the reporting period. This is the balance of account 42 at the beginning of the period.

Np- margin on the goods received (monthly turnover on the credit of account 42).

Hb- margin on retired goods (monthly debit turnover on account 42). Retired goods are those that have documentary evidence: return to the supplier, cancellation of defects, etc.

OK- balance at the end of the period (balance account 41.2)

Example. In accounting, the balances on account 41.2 are 80 thousand, on account 40 - 15,514. Goods received for the period are 120 thousand rubles, the margin on them is 27,692. Revenue for this period is 165 thousand rubles. There were no out-of-stock items. The balance of goods at the end of the reporting period is 35 thousand rubles.

P \u003d (15,514 + 27,692) / (165,000 + 35,000)) * 100% \u003d 21.6%

VD \u003d 165,000 * 21.6% \u003d 35,640 rubles.

The method is rarely used, since the amount of the accrued, realized margin for all items is required. If it is possible to account for certain goods, then it is better to keep accounting at purchase prices.

Gross income:

VD \u003d Nn + Np-Nv-Nk

Hn- markup at the beginning of the period on balances: balance account. 42;

Np- mark-up of goods arrived for the reporting period: credit turnover c. 42;

Hb-mark-up on retired goods: debit turnover account. 42;

Hk- markup at the end of the period for the balance: balance account. 42.

When calculating, you will need to use the data of all expenditure items, if available. The complexity of the calculation is that it is required to include all income and a number of production costs, the cost price.

Timely and high-quality accounting will greatly simplify the calculation of gross profit. You can quickly find the required items of expenses and income in it.

Not everyone has an accurate understanding of the concept of the gross profit of the enterprise. It is often confused with accounting profit.

VP- income from the sale of products, which is calculated through retention from total amount proceeds after the sale of goods VAT, expenses and excise taxes for production and sale, included in the cost. The main part of VP consists of sales revenue.

Accounting profit - the combined gross profit, a favorable financial outcome, which is calculated from the accounting records of the organization for the required period. When determining it, all business procedures and balance sheet items are taken into account.

Accounting profit is based on two theses:

There are several views on the concept of "income". Some consider it an increase in income financial resources during the calculated period from the funds invested by the founders, a consequence of the improvement of well-being. This definition was based on the thesis of A. Smith: income is the amount spent without attempts on a part of the fixed capital.

The stated thesis was called the idea of profit formed on changes in the balance of the organization: liabilities - sources, assets - resources. The method is effective only with an increase in assets or a reduction in liabilities, costs - on the contrary. income is growth financial resources, and losses - reduction.

The second concept of income is the quantitative difference between the profit received and the expenses incurred. Income becomes the result of a competent distribution of revenue and costs over periods. Profit becomes an asset and costs a liability even in future periods. This is the basis of the double entry in accounting, which forms a double financial result.

Accounting profit is the difference between IA and external costs:

PB = VD - IV

PB- accounting profit;

VD- the annual income of the organization as a result of economic activity in monetary terms (the difference between revenue and costs incurred to receive);

IV- the cost of manufacturing products (cost) - wages, material costs, loans.

External costs will be passed on to the consumer of the product.

Economic profit - the income remaining for the organization after withholding the obvious and implicit costs.

P \u003d SD - I

P- profit;

And- total costs;

SD- total income.

Serious errors in the calculation appear when a person confuses the classical profit with the gross. A video will help you avoid mistakes, where an economist will explain all the features of these two different concepts.

Calculating gross profit every month or quarter is impractical and meaningless. The data does not show the real situation. As a rule, calculations are carried out once a year.

You should be careful about the distribution of VP in the organization, as this will improve, increase the capacity of the enterprise, increase the potential of employees, increase net profit in future. The main thing will be the construction of the trading process rationally and cost-effectively.

Each company is aimed at obtaining the greatest efficiency as a result of its activities. More specifically, profit. But it is impossible to determine it without such an indicator as gross profit. Let's tell you what it is in simple words, we give calculation formulas and examples.

Gross profit is the difference between the company's revenue and cost products sold(services), but without deducting income tax. But if we consider official term words, it is enshrined only in the Methodological recommendations for accounting of agricultural and other enterprises of the agro-industrial complex (approved by order of the Ministry of Agriculture dated January 31, 2003 No. 28). So literally from paragraph 49 of the Methodological recommendations it follows that:

"gross profit is defined as the difference between the proceeds from the sale of products, goods, works and services and the sum of the cost of their sale."

However, in practice, the extended interpretation is rarely used. The concept of gross profit is simplified for easier perception. Therefore, in various sources there are such concepts of gross profit as:

Which of these concepts to apply is not important. The main thing is to correctly calculate the indicator.

When calculating, it is important to separate the concepts of net and gross profit. As previously noted, gross profit is the difference between revenue and production costs. For example, such as for the purchase of raw materials, materials, staff salaries, etc.

Calculating production costs is a rather laborious process. Since it is necessary to take into account both significant expenses and insignificant expenditures of money. For example, do not forget to include debts on loans, loans, insurance premiums, fines, and rent payments. After all the transactions related to payments, you will receive an indicator of net profit.

As a result, net profit is a part of gross profit, but net of taxes and other liabilities. Its managers spend at their discretion, for example, on the modernization of assets, or replenishment of working capital.

To understand the differences between the two indicators, see the table below.

Table. The main differences between net and gross profit

| Gross profit | Net profit |

|

|

| The indicator is equal to the difference between revenue and expenses, which reflect the cost of production | The indicator is equal to the difference between gross profit and the amount of taxes transferred to the budget |

| Reflects business performance | Reflects the efficiency of accounting and tax accounting |

The calculation of gross profit depends on the activities of the company. However, there is a general formula for calculating gross profit. We have reflected it below.

VP \u003d D - (S + W) , where

VP - the amount of gross profit;

D - the number of manufactured goods sold (in value terms);

C - the cost of manufacturing goods;

Z - production costs.

VP \u003d B (line 2110) - SR (line 2120) , where

B - revenue;

SR - cost of sales.

To make accurate calculations, check all expenses in detail. In particular, those that were incurred for the manufacture and sale of products. Some companies use turnover based calculations. For example, when one markup is set for different product ranges. It is convenient to use such a calculation, since the value of the turnover is taken. That is, the final income, taking into account the calculated VAT.

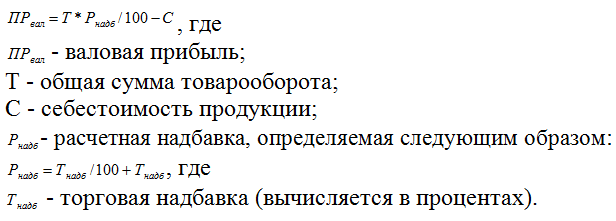

VP \u003d TxPH / 100-C , where

VP - gross income;

T - the result of the turnover;

C - the cost of inventory items;

РН - estimated allowance.

Gross profit is considered before the final tax liability is determined. Moreover, the calculation itself depends on what kind of activity your company conducts:

Sale of goods : Calculate the total income. Then, determine the amount of net profit. To do this, subtract from the total amount all the costs incurred by you for the return of defective products and discounts to customers. Next, subtract the cost of production from the resulting indicator - this is the gross profit.

Provide services : Gross revenue equals net income. Therefore, to calculate the total amount, determine the difference between the income received and spending on discounts, elimination of defects and shortcomings in the service provided.

In addition, when calculating, check whether the indicators are reliably reflected in the cash receipt statements. And regardless of whether it is cash or non-cash transfers. Also consider the cost of purchasing goods and materials, cars, real estate and office equipment and appliances.

Lastly, analyze the correctness of the calculations. To do this, divide the amount of gross profit by net profit. The final percentage is the difference between the cost of inventory and the price tag when they are sold. And finally, consider additional sources of revenue. When you receive income other than from your main activity, add the amount to your gross income. The result is gross revenue.

For clarity, consider an example of how to calculate gross revenue and analyze it. LLC "Company - 1" and LLC "Company - 2" are engaged in the production of bakery products. 1 company is located in Moscow, where its main sales market, and 2 - in Yekaterinburg. But she has a different assortment of bakery products. Therefore, we are interested in the gross profit of LLC "Company - 1", see its performance in the table.

Table. Calculation of the gross profit of LLC "Company - 1" for 6 months of 2019

| Name/month | 1 | 2 | 3 | 4 | 5 | 6 | Total |

| Revenue, thousand rubles | 2989 | 3330 | 3444 | 3797 | 5017 | 4885 | 23 463 |

| Cost of sales, thousand rubles | 978 | 1077 | 1165 | 1310 | 1542 | 1572 | 7644 |

| Gross profit, thousand rubles | 2012 | 2253 | 2279 | 2488 | 3476 | 3313 | 15819 |

| Gross profit margin, % | 67,3% | 67,6% | 66,2% | 65,5% | 69,3% | 67,8% | 67,4% |

The table shows that every month the gross profit of LLC "Company - 1" increases. Its revenue for the six months of 2019 amounted to 23.4 million rubles, and the cost of sales - 7.6 million rubles. Therefore, the final gross profit is 15.8 million rubles, and the average for the month is 2.6 million rubles. (15.8:6 months). That is, funds that can cover the rest of the costs. For example, for management needs, interest on loans, etc.

Despite the fact that the indicators are quite significant, it is impossible to unambiguously say from them whether the company is working effectively or not. Therefore, we calculate the profitability of gross profit. This is the ratio of gross profit to the company's revenue. And so, for half a year it is equal to 67.4%, but in March and April it decreases. This is due to the introduction of a new type of product into production. Their prime cost is quite high from March to May, as the company did not pass by the volume of purchases for the preferential cost of raw materials and materials. But in July, the situation changed dramatically.